30+ Companies Affected by One Strait

Between March 3 and March 17, 2026, 30+ publicly listed Indian companies filed disclosures acknowledging operational disruptions tied to LPG, LNG, and petrochemical feedstock shortages linked to the conflict. Some of those disclosures were four sentences long. A few were specific about operational timelines. Most used the standard regulatory language of force majeure and estimated impact disclaimers.

Read together, they describe an industrial economy with a concentrated dependency on a single energy corridor one that came under pressure faster than most models had anticipated.

This article compiles what the filings say, maps the operational and financial impact across sectors, and identifies the variables that will determine how quickly conditions normalize.

How a Chokepoint Became a Crisis

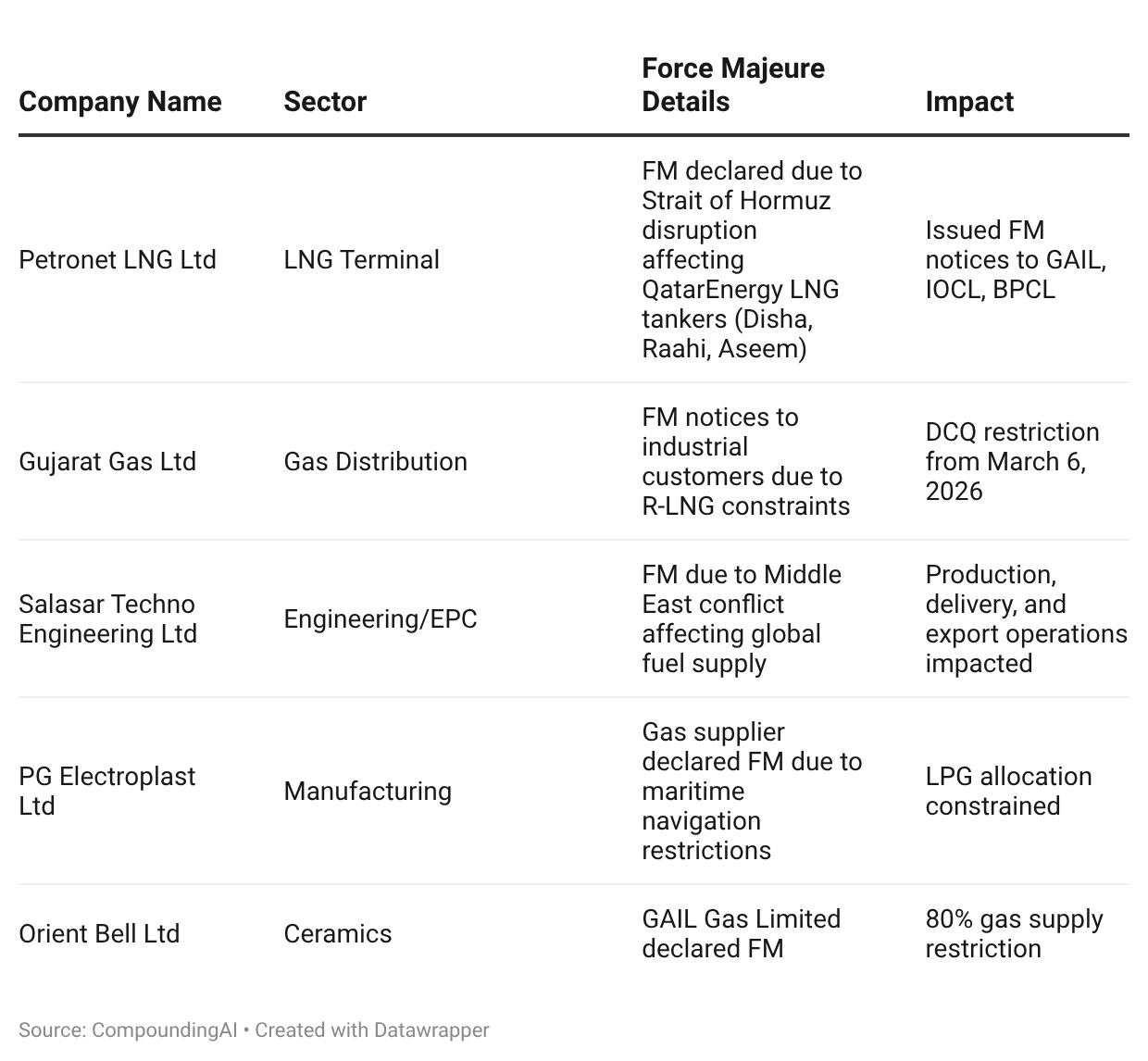

The Strait of Hormuz carries roughly 20% of global oil consumption every single day. When the conflict escalated in late February, three QatarEnergy LNG tankers : Disha, Raahi, and Aseem were caught up in navigation restrictions. Petronet LNG, India’s largest LNG terminal operator, declared Force Majeure on its Qatar contracts. The cascade began from there.

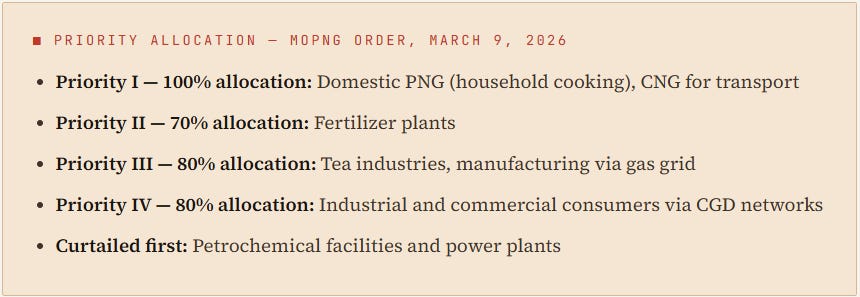

What followed was essentially a domino chain. With LNG supply constrained, India’s oil marketing companies faced a domestic LPG supply crunch. The Ministry of Petroleum and Natural Gas moved fast, on March 9, it issued the Natural Gas (Supply Regulation) Order, 2026, which set a strict priority framework for who gets gas and how much.

| Priority Level | Allocation | Targeted Sector/Consumer |

|---|---|---|

| Priority I | 100% | Domestic PNG (household cooking), CNG for transport |

| Priority II | 70% | Fertilizer plants |

| Priority III | 80% | Tea industries, manufacturing via gas grid |

| Priority IV | 80% | Industrial and commercial consumers via CGD networks |

| Curtailed First | N/A | Petrochemical facilities and power plants |

{kind=link}

That last line, “curtailed first”, is where the real story lives. The government essentially told the petrochemical sector: you are last in the queue. And the companies that depended on propylene or LPG as their primary feedstock, not just as fuel, had nowhere to turn.

CPCL stopped supplying propylene to Manali Petrochemicals. HPCL stopped supplying propylene to Andhra Petrochemicals. BPCL discontinued LPG supply to Hindustan Organic Chemicals at Kochi. Each of these decisions flowed from the same upstream directive: refinery output had to be diverted toward domestic LPG production. The downstream casualties were predictable in hindsight. They just weren’t in anyone’s earnings model.

“The PRU unit is compelled to temporarily shut down operations on March 9, 2026, with all other down-the-line units following suit within 2 days.”— Hindustan Organic Chemicals Ltd, BSE Filing

The Damage Map: 30+ Companies, Six Sectors

The affected companies fall into three broad buckets, and it helps to think about them separately because the investment implications are completely different.

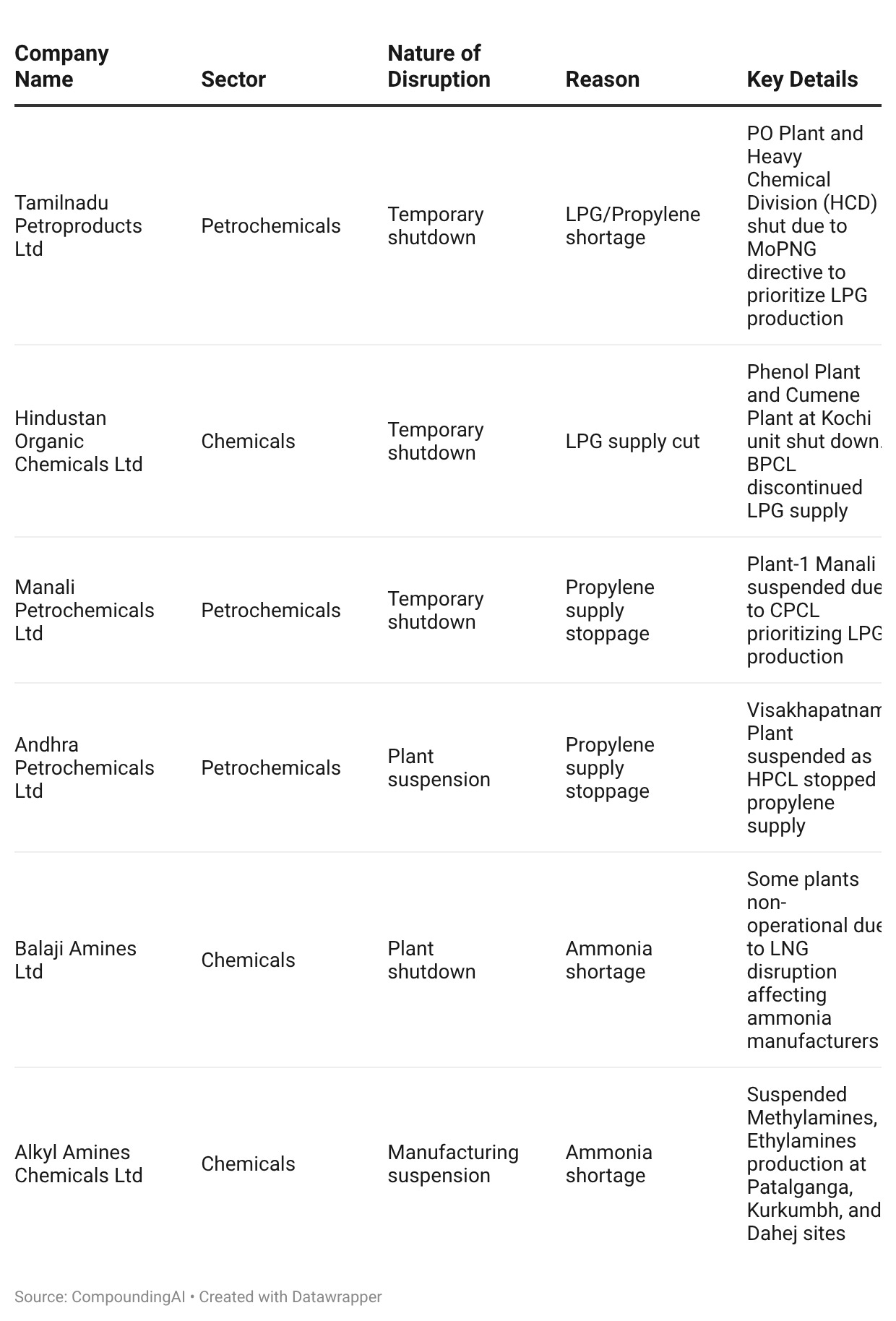

The first bucket is the hardest hit: petrochemical and amine manufacturers who use LPG or propylene not as fuel but as their core raw material. For them, this it was a production stoppage. Tamilnadu Petroproducts shut its PO Plant and Heavy Chemical Division. HOCL shut its Phenol and Cumene plants. Manali Petrochemicals suspended Plant-1. Andhra Petrochemicals suspended its entire Visakhapatnam facility. Balaji Amines and Alkyl Amines suspended methylamine and ethylamine production across multiple sites. These are complete shutdowns, not rationalisations.

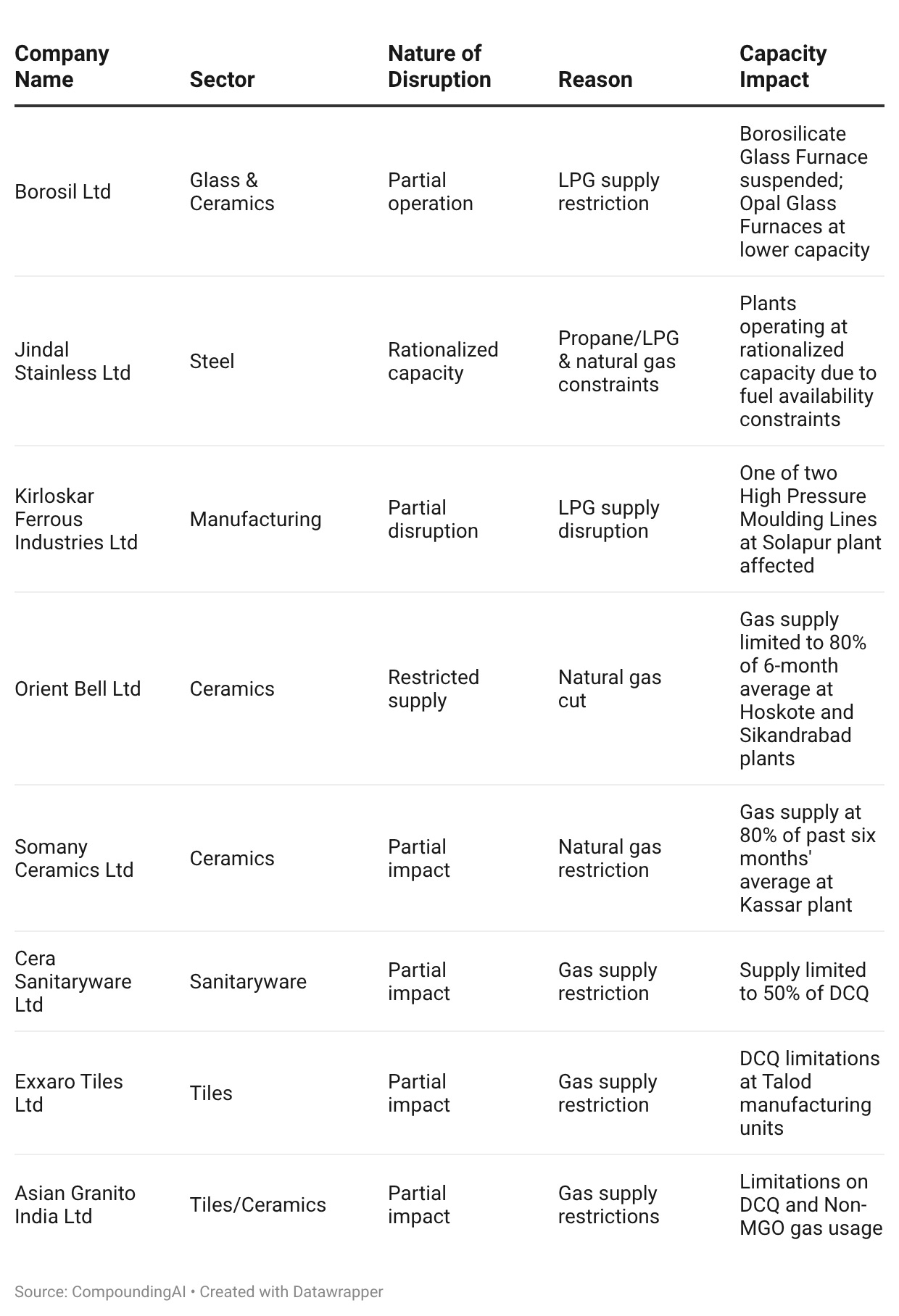

The second bucket is the ceramics, tiles, and glass sector, companies that use natural gas as kiln or furnace fuel. They received a 50–80% gas supply restriction rather than a full cutoff, which means they’re operating below capacity rather than stopped entirely. Orient Bell, Somany Ceramics, Cera Sanitaryware, Exxaro, Asian Granito, and Borosil all filed disclosures describing “limitations on DCQ”, contractual daily quantity restrictions with varying degrees of operational impact depending on plant location and fuel flexibility.

The third bucket is the gas distribution companies: Gujarat Gas, Adani Total Gas, Mahanagar Gas. The government order restricts their industrial and commercial volumes to 80%, but explicitly protects domestic PNG and CNG at 100%. The operational disruption for CGD companies is therefore concentrated in the industrial segment, while their household and transport fuel businesses continue unaffected. Tatva Chintan Pharma Chem and Bosch Home Comfort India also fall into this regulatory category, both operating under the pooled price and gas allocation mechanisms established by the MoPNG order.

A fourth category covers supply chain and logistics disruptions rather than direct gas or feedstock shortages. Precision Wires India flagged re-routing costs on import and export shipments. IndiGo cancelled over 500 flights due to airspace restrictions and separately introduced a fuel surcharge of ₹425–₹2,300 per sector following the sharp rise in aviation turbine fuel prices. Salasar Techno Engineering and PG Electroplast also filed force majeure declarations on the basis of disruptions from their upstream gas suppliers rather than direct feedstock dependency.

Finally, three companies filed disclosures that described minimal or no material impact. Carysil’s dual-fuel capability, PNG and LDO, insulated its manufacturing operations, and 90% of its exports are on FOB terms, limiting freight exposure. Hindalco reported less than 0.1% of operations affected, aided by captive power arrangements.

Reliance Industries, as an upstream refiner, was on the other side of the equation, directed to maximise LPG production to support domestic supply, which placed it in the position of a contributor to the government’s priority allocation framework rather than a recipient of its restrictions.

Table 1 — Companies with Complete or Temporary Shutdowns

{kind=link}

| Company Name | Sector | Nature of Disruption | Reason | Key Details |

|---|---|---|---|---|

| Tamilnadu Petroproducts Ltd | Petrochemicals | Temporary shutdown | LPG/Propylene shortage | PO Plant and Heavy Chemical Division (HCD) shut due to MoPNG directive to prioritize LPG production |

| Hindustan Organic Chemicals Ltd | Chemicals | Temporary shutdown | LPG supply cut | Phenol Plant and Cumene Plant at Kochi unit shut down. BPCL discontinued LPG supply |

| Manali Petrochemicals Ltd | Petrochemicals | Temporary shutdown | Propylene supply stoppage | Plant-1 Manali suspended due to CPCL prioritizing LPG production |

| Andhra Petrochemicals Ltd | Petrochemicals | Plant suspension | Propylene supply stoppage | Visakhapatnam Plant suspended as HPCL stopped propylene supply |

| Balaji Amines Ltd | Chemicals | Plant shutdown | Ammonia shortage | Some plants non-operational due to LNG disruption affecting ammonia manufacturers |

| Alkyl Amines Chemicals Ltd | Chemicals | Manufacturing suspension | Ammonia shortage | Suspended Methylamines, Ethylamines production at Patalganga, Kurkumbh, and Dahej sites |

Table 2 — Companies with Partial / Reduced Operations

{kind=link}

| Company Name | Sector | Nature of Disruption | Reason | Capacity Impact |

|---|---|---|---|---|

| Borosil Ltd | Glass & Ceramics | Partial operation | LPG supply restriction | Borosilicate Glass Furnace suspended; Opal Glass Furnaces at lower capacity |

| Jindal Stainless Ltd | Steel | Rationalized capacity | Propane/LPG & natural gas constraints | Plants operating at rationalized capacity due to fuel availability constraints |

| Kirloskar Ferrous Industries Ltd | Manufacturing | Partial disruption | LPG supply disruption | One of two High Pressure Moulding Lines at Solapur plant affected |

| Orient Bell Ltd | Ceramics | Restricted supply | Natural gas cut | Gas supply limited to 80% of 6-month average at Hoskote and Sikandrabad plants |

| Somany Ceramics Ltd | Ceramics | Partial impact | Natural gas restriction | Gas supply at 80% of past six months' average at Kassar plant |

| Cera Sanitaryware Ltd | Sanitaryware | Partial impact | Gas supply restriction | Supply limited to 50% of DCQ |

| Exxaro Tiles Ltd | Tiles | Partial impact | Gas supply restriction | DCQ limitations at Talod manufacturing units |

| Asian Granito India Ltd | Tiles/Ceramics | Partial impact | Gas supply restrictions | Limitations on DCQ and Non-MGO gas usage |

Table 3 — Force Majeure Declarations

| Company Name | Sector | Force Majeure Details | Impact |

|---|---|---|---|

| Petronet LNG Ltd | LNG Terminal | FM declared due to Strait of Hormuz disruption affecting QatarEnergy LNG tankers (Disha, Raahi, Aseem) | Issued FM notices to GAIL, IOCL, BPCL |

| Gujarat Gas Ltd | Gas Distribution | FM notices to industrial customers due to R-LNG constraints | DCQ restriction from March 6, 2026 |

| Salasar Techno Engineering Ltd | Engineering/EPC | FM due to Middle East conflict affecting global fuel supply | Production, delivery, and export operations impacted |

| PG Electroplast Ltd | Manufacturing | Gas supplier declared FM due to maritime navigation restrictions | LPG allocation constrained |

| Orient Bell Ltd | Ceramics | GAIL Gas Limited declared FM | 80% gas supply restriction |

{kind=link}

What the Filings Actually Say

Indian regulatory filings during supply disruptions follow a recognizable pattern. The phrase “likely impact cannot be estimated at this time” is standard legal language that appears across almost every disclosure in this set. Reading past that boilerplate, three details from these filings stand out as materially significant.

HOCL’s inventory disclosure is unusually specific. The company stated its buffer stock would be “fully utilized by evening of March 9”, the same day the MoPNG order was issued. This is a narrower operational window than most disruption filings describe. HOCL is dependent on BPCL for LPG feedstock, and the filing does not reference any alternate supplier arrangement. The Phenol and Cumene plants are stopped pending supply restoration, with the timeline entirely contingent on OMC decisions upstream.

Cera Sanitaryware’s characterization of the disruption as “not material” sits alongside reported data showing a 50% gas supply restriction and a Q3 FY26 EBITDA margin of 10.2% against 13.2% in the prior year, a 300 basis point compression. The company does have meaningful mitigating factors: zero debt, ₹757 crore in cash, and an alternative supply arrangement with GAIL. Whether the characterization ultimately proves accurate will depend on how long the restriction continues and how much volume the GAIL arrangement restores. It is a data point worth tracking against Q4 disclosures.

Petronet LNG’s disclosure on business interruption insurance carries broad implications. The company noted that “Acts of War are excluded under Business Interruption Insurance covers.” Several other companies in this set have declared Force Majeure events tied to the same conflict. If insurers classify the disruption as an act of war which is a standard exclusion in most BI policies, companies expecting insurance coverage to partially offset losses may not receive it. This is a material uncertainty that is not yet reflected in most of the impact estimates circulating in the market.

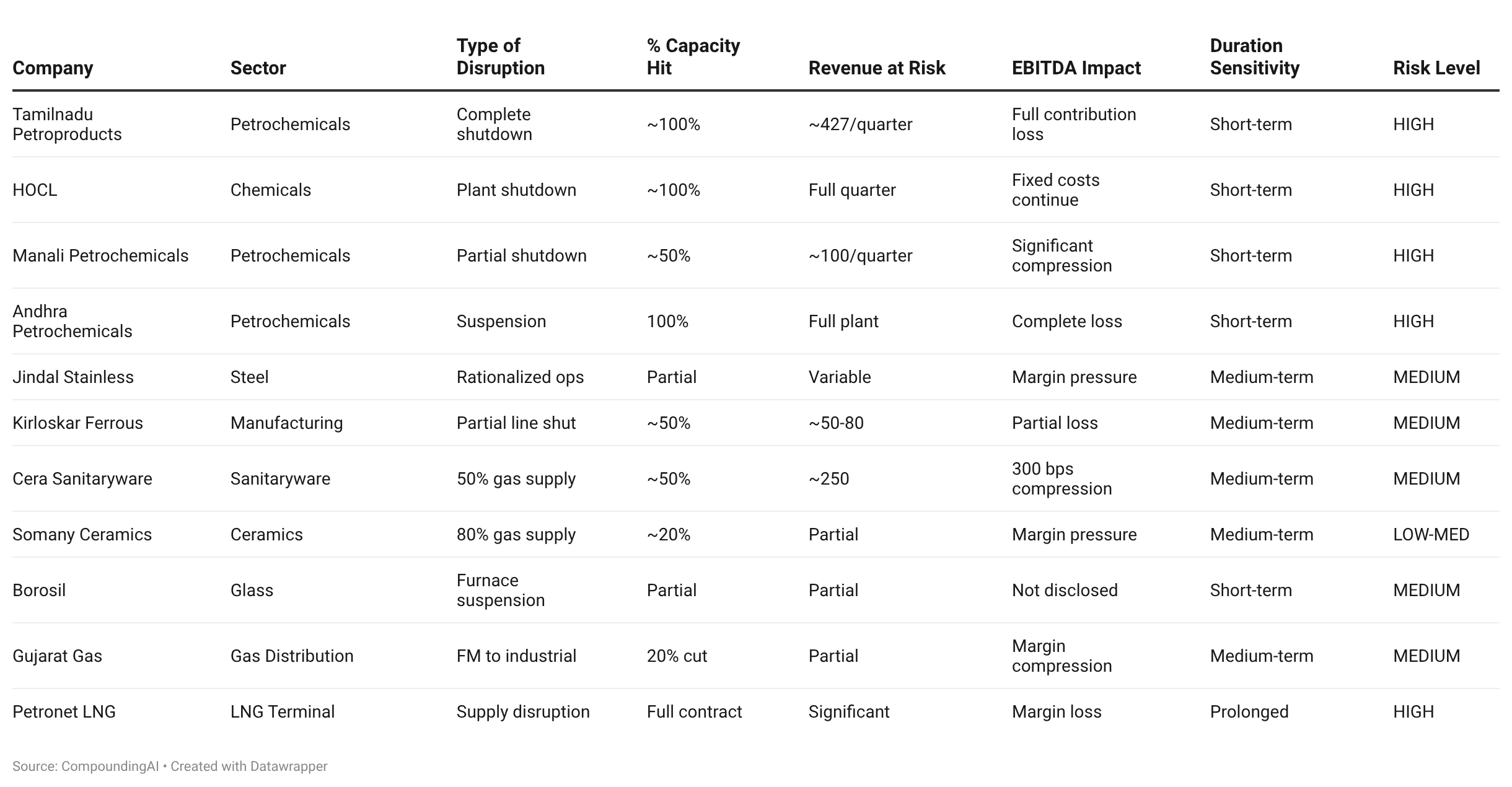

The Numbers: What’s Actually at Risk

Table 4 — Quantified Impact Assessment

| Company | Sector | Type of Disruption | % Capacity Hit | Revenue at Risk | EBITDA Impact | Duration Sensitivity | Risk Level |

|---|---|---|---|---|---|---|---|

| Tamilnadu Petroproducts | Petrochemicals | Complete shutdown | \~100% | \~427/quarter | Full contribution loss | Short-term | HIGH |

| HOCL | Chemicals | Plant shutdown | \~100% | Full quarter | Fixed costs continue | Short-term | HIGH |

| Manali Petrochemicals | Petrochemicals | Partial shutdown | \~50% | \~100/quarter | Significant compression | Short-term | HIGH |

| Andhra Petrochemicals | Petrochemicals | Suspension | 100% | Full plant | Complete loss | Short-term | HIGH |

| Jindal Stainless | Steel | Rationalized ops | Partial | Variable | Margin pressure | Medium-term | MEDIUM |

| Kirloskar Ferrous | Manufacturing | Partial line shut | \~50% | \~50-80 | Partial loss | Medium-term | MEDIUM |

| Cera Sanitaryware | Sanitaryware | 50% gas supply | \~50% | \~250 | 300 bps compression | Medium-term | MEDIUM |

| Somany Ceramics | Ceramics | 80% gas supply | \~20% | Partial | Margin pressure | Medium-term | LOW-MED |

| Borosil | Glass | Furnace suspension | Partial | Partial | Not disclosed | Short-term | MEDIUM |

| Gujarat Gas | Gas Distribution | FM to industrial | 20% cut | Partial | Margin compression | Medium-term | MEDIUM |

| Petronet LNG | LNG Terminal | Supply disruption | Full contract | Significant | Margin loss | Prolonged | HIGH |

{kind=link}

Aggregating across the petrochemicals sector, the disclosures point to ₹800-1,200 crore in quarterly EBITDA at risk under a full-quarter shutdown scenario. Ceramics and tiles contribute an estimated ₹150-250 crore in margin compression. Steel adds another ₹200-400 crore. For larger diversified companies like Jindal Stainless, the absolute impact is a smaller share of the overall business. For companies like HOCL and Andhra Petrochemicals, where affected divisions represent the core of their operations, the relative exposure is considerably more significant.

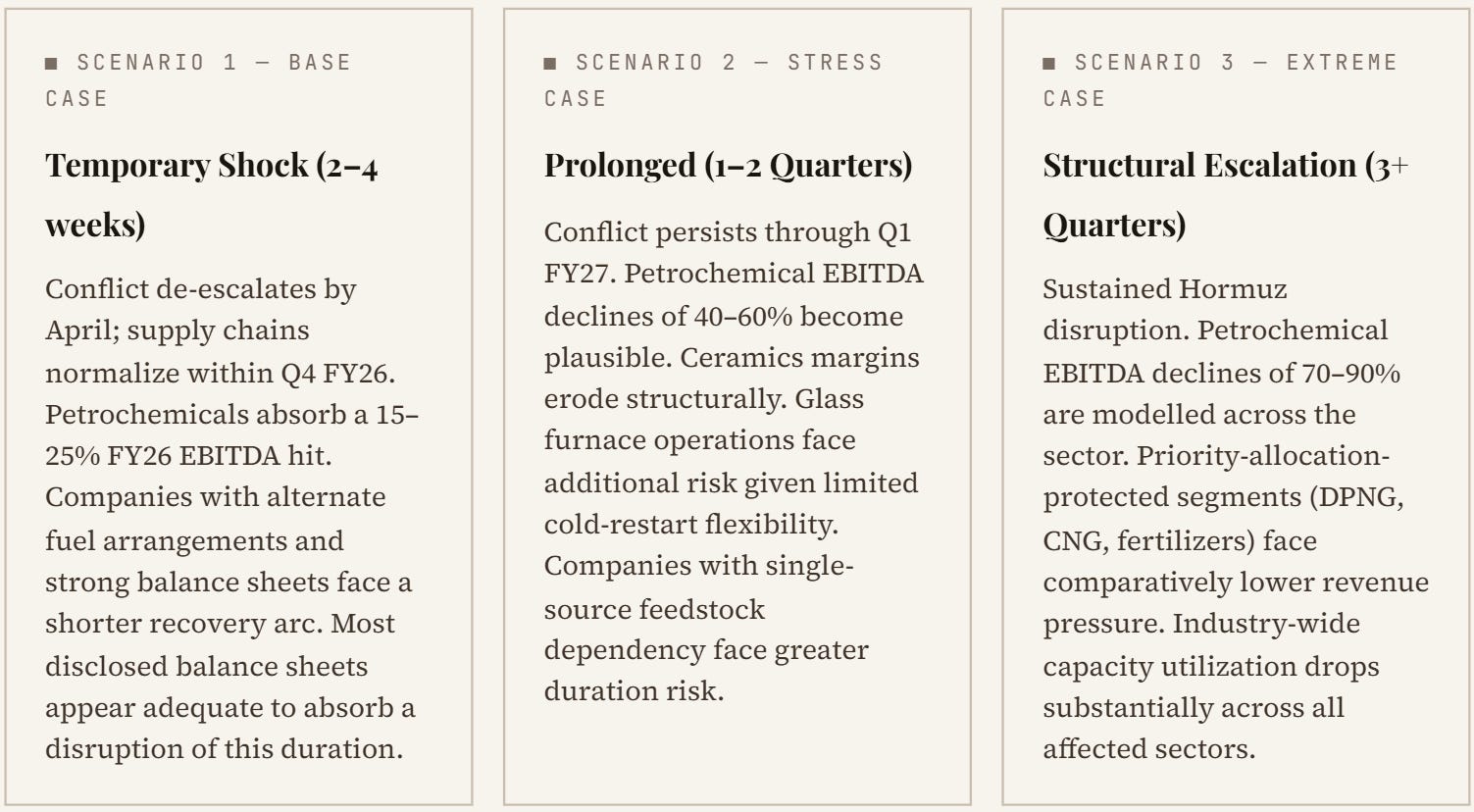

Three Scenarios for What Happens Next

| Scenario | Duration | Expected Outlook | Sectoral Impact |

|---|---|---|---|

| Scenario 1 - Base Case | Temporary Shock (2–4 weeks) | Conflict de-escalates by April; supply chains normalize within Q4 FY26. | Petrochemicals absorb a 15–25% FY26 EBITDA hit. Companies with alternate fuel and strong balance sheets recover quickly. |

| Scenario 2 - Stress Case | Prolonged (1–2 Quarters) | Conflict persists through Q1 FY27. | Petrochemical EBITDA declines of 40–60% plausible. Ceramics margins erode; Glass faces cold-restart risks. Single-source feedstock users face high risk. |

| Scenario 3 - Extreme Case | Structural Escalation (3+ Quarters) | Sustained Hormuz disruption. | Petrochemical EBITDA declines of 70–90%. Industry-wide capacity drops. Protected segments (DPNG, CNG, Fertilizers) face lower revenue pressure. |

{kind=link}

The duration of the MoPNG order is the most important variable to monitor. If the Natural Gas Supply Regulation Order is extended through April without modification, that signals the government does not anticipate near-term supply normalization. Conversely, any upward revision to industrial allocation thresholds would indicate conditions improving upstream.

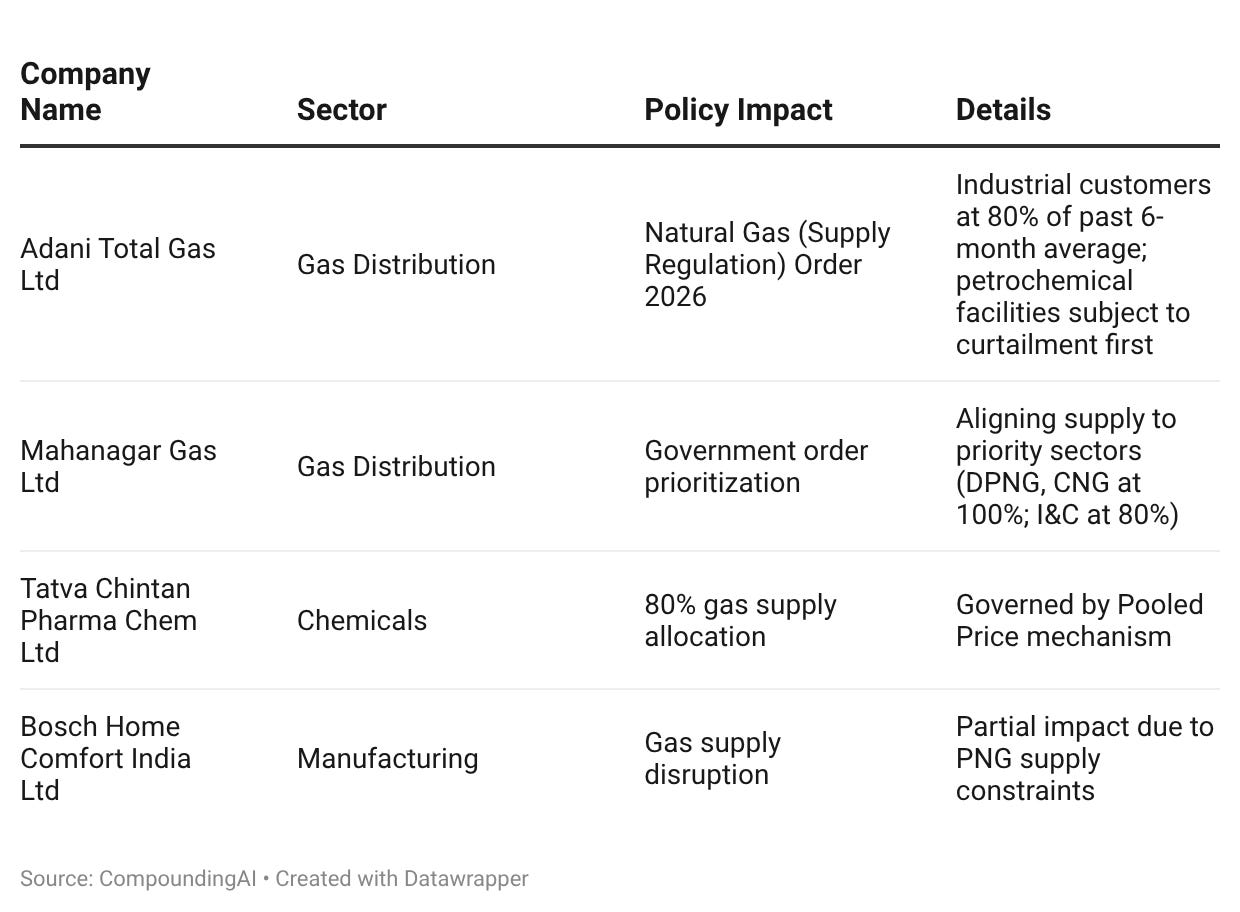

Table 5 — Companies Impacted by Regulatory / Policy Changes

| Company Name | Sector | Policy Impact | Details |

|---|---|---|---|

| Adani Total Gas Ltd | Gas Distribution | Natural Gas (Supply Regulation) Order 2026 | Industrial customers at 80% of past 6-month average; petrochemical facilities subject to curtailment first |

| Mahanagar Gas Ltd | Gas Distribution | Government order prioritization | Aligning supply to priority sectors (DPNG, CNG at 100%; I\&C at 80%) |

| Tatva Chintan Pharma Chem Ltd | Chemicals | 80% gas supply allocation | Governed by Pooled Price mechanism |

| Bosch Home Comfort India Ltd | Manufacturing | Gas supply disruption | Partial impact due to PNG supply constraints |

{kind=link}

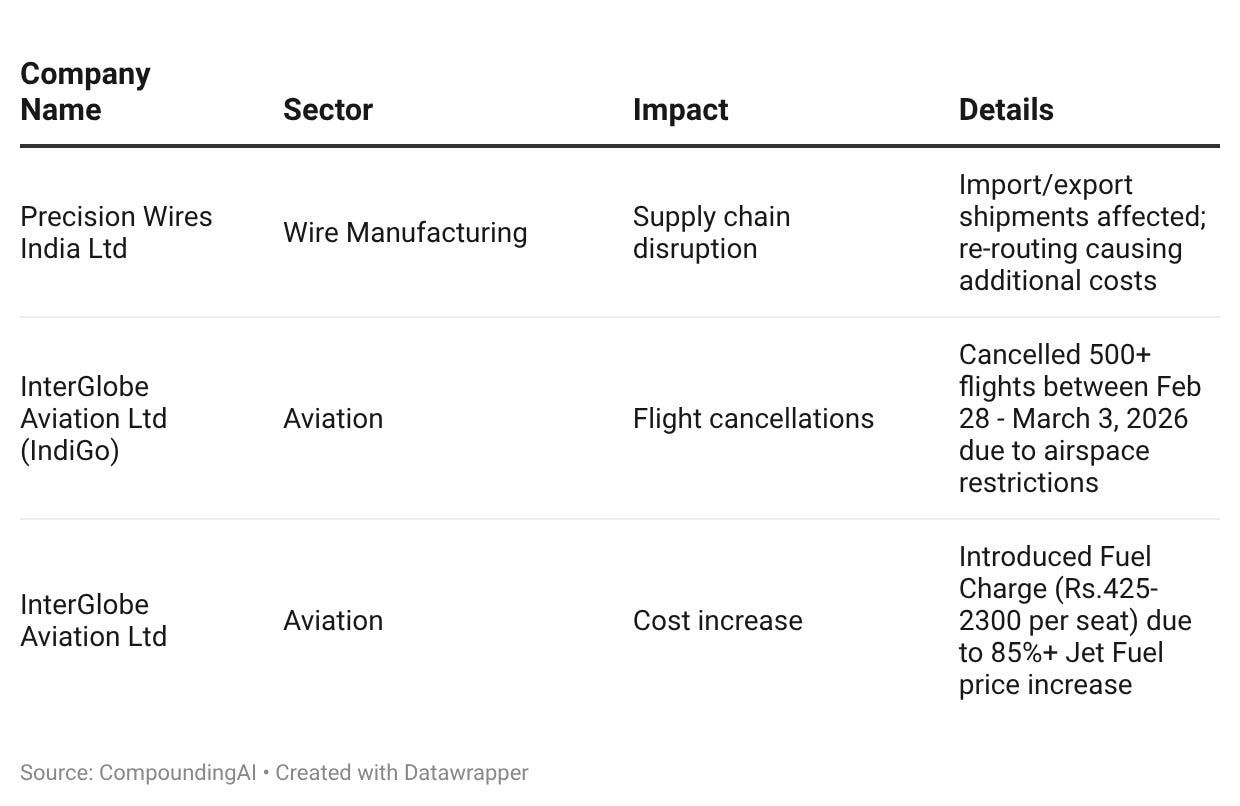

Table 6 — Companies with Supply Chain / Logistics Impact

{kind=link}

| Company Name | Sector | Impact | Details |

|---|---|---|---|

| Precision Wires India Ltd | Wire Manufacturing | Supply chain disruption | Import/export shipments affected; re-routing causing additional costs |

| InterGlobe Aviation Ltd (IndiGo) | Aviation | Flight cancellations | Cancelled 500+ flights between Feb 28 - March 3, 2026 due to airspace restrictions |

| InterGlobe Aviation Ltd | Aviation | Cost increase | Introduced Fuel Charge (Rs. 425–2300 per seat) due to 85%+ Jet Fuel price increase |

Table 7 — Companies Reporting Minimal Impact / Continuing Normal Operations

| Company Name | Sector | Status | Details |

|---|---|---|---|

| Carysil Ltd | Kitchenware | Operations normal | Dual fuel capability (PNG and LDO); 90% exports on FOB basis |

| Hindalco Industries Ltd | Aluminum | Minimal impact | Less than 0.1% of operations affected; captive power arrangements |

| Reliance Industries Ltd | Conglomerate | Maximizing LPG production | Proactively maximizing LPG production to ensure domestic supply |

{kind=link}

The gap worth noting across these filings is between management language and disclosed operational facts. Multiple companies use the phrase “likely impact cannot be estimated” while simultaneously describing complete production stoppages. This is standard legal disclaimer language, but it leaves the operational picture to be read between the lines rather than stated directly.

Cera’s description of a 50% gas supply restriction as “not material” sits alongside reported margin data showing 300 bps compression, the company has meaningful mitigating factors (zero debt, ₹757 crore in cash, a GAIL alternative arrangement), but the characterisation of the disruption itself is one to track against Q4 disclosures.

“Clarity from the Government on allocation percentage for industrial propane/LPG and natural gas is crucial for the stainless steel industry to plan operations.”— Jindal Stainless Ltd, Management Statement

What to Watch

Three data points will shape how this situation develops over the next sixty days. First, the MoPNG order: any revision to industrial gas allocation percentages, upward or downward, will be the clearest signal of how the government is reading supply conditions. Second, restart announcements from the petrochemical shutdowns: the timing and language around restarts at TPL, HOCL, Manali, and Andhra Petrochemicals will indicate how quickly the propylene and LPG supply chain is normalizing. Third, Q4 FY26 earnings: this will be the first quarter where the full financial impact is captured in reported numbers rather than qualitative disclosures. The “cannot estimate” language in current filings will need to be replaced with actual figures.

A broader question the situation raises is structural. India’s industrial gas supply chain proved vulnerable to a geopolitical event affecting a single shipping corridor in under two weeks, from tanker disruption to plant shutdown. The government’s priority allocation framework responded quickly, but the speed of propagation underscores how concentrated the dependencies are. Whether this accelerates policy attention toward energy supply diversification is a medium-term question that extends well beyond any single quarter’s earnings impact.

Thirty plus companies filed operational disruption disclosures in the span of two weeks because LNG tankers could not complete their transit through a fifty-four kilometre strait. The full financial picture will only become clear in April earnings and the quarter after that.

Until then, the filings themselves are the most reliable source of information available.

Note : Not a buy/sell recommendation. For education purposes only.

This article is created using inputs only from CompoundingAI.

CompoundingAI is a vertical intelligence engine that transforms unstructured documents into decision-grade insights, complete with source-level traceability for confident, auditable workflows. We cut the noise & directly deliver insights.

Powered by CompoundingAI — AI research platform for Indian stocks, every claim cited from primary filings

Login Now