Fermenta Biotech: From Collapse to Comeback

Introduction: The Vitamin D₃ King

Some companies dominate headlines because of their sheer size. Others because of their controversies. Fermenta Biotech falls into neither camp. For decades, it quietly supplied Vitamin D₃ to the world, a product most of us encounter daily in fortified milk, multivitamins, or animal feed, without realizing that an Indian company was behind it.

The firm isn’t glamorous like a biotech innovator promising the next cancer cure, nor as familiar as a pharma giant like Sun or Dr. Reddy’s. Instead, Fermenta lives in the niche, where chemistry meets biology, producing specialized molecules that end up in everything from supplements to waste treatment plants.

But over the past five years, Fermenta’s journey has been anything but dull. Margins collapsed, debt piled up, and an over-reliance on animal feed markets dragged performance into the red. And yet in FY25 the company staged a dramatic turnaround. Raw material costs fell, profitability surged, and its environmental solutions business spun out into a dedicated subsidiary.

And with Q1 FY26 results, the turnaround theory looks picking momentum. Revenues jumped 74% YoY, margins touched multi-year highs, and the crown jewel Vitamin D₃ business is once again pulling the cart.

So what exactly is Fermenta Biotech today? What drives its revenue, where are the risks, and how sustainable is its comeback? Let’s walk through the numbers and the narrative, piece by piece.

1. The Core Business Model: Vitamin D₃ at the Center

Financial Highlights

{kind=link}

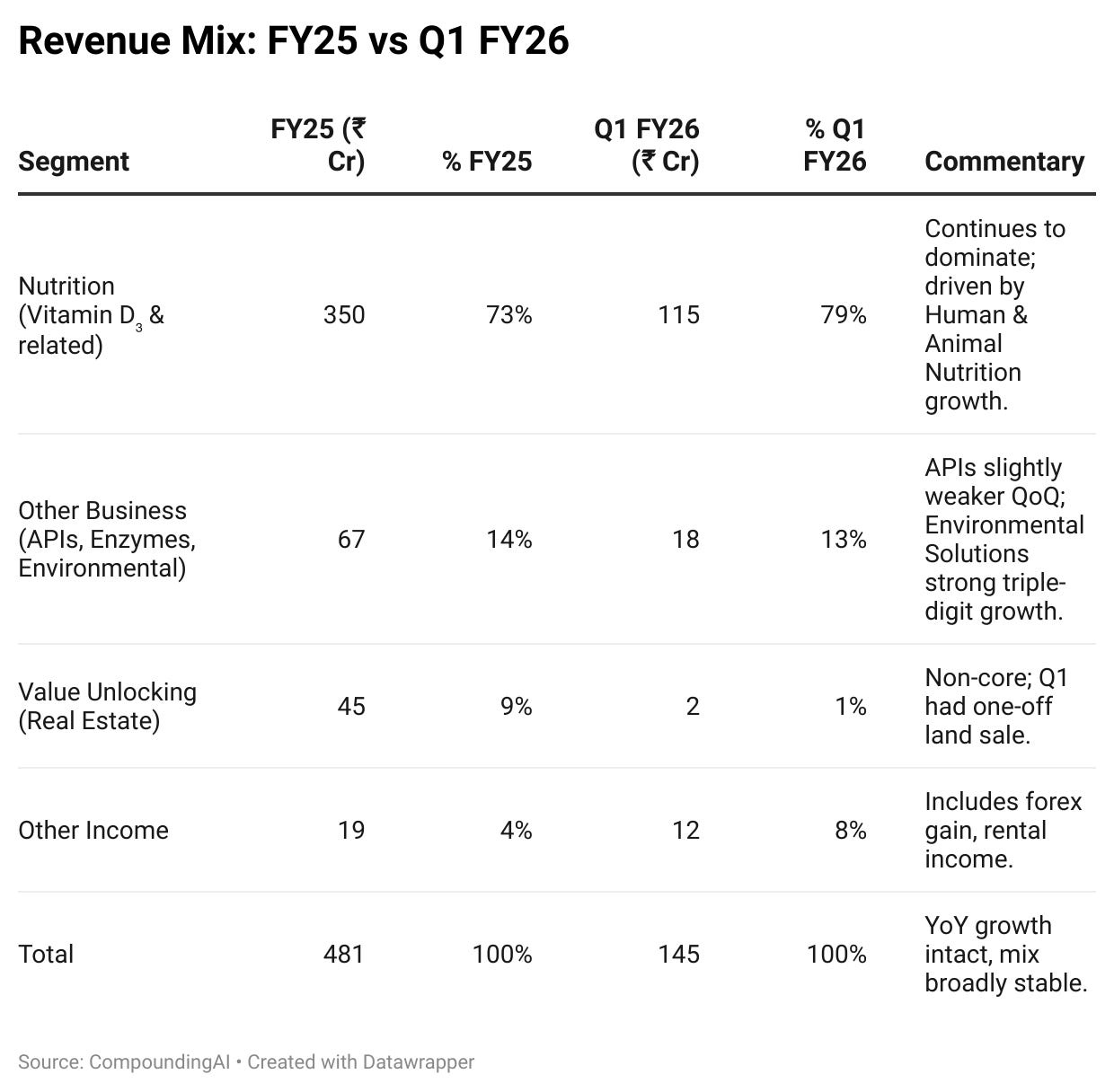

Fermenta Biotech is not a diversified conglomerate, its crown jewel is Vitamin D₃. But that crown jewel is surrounded by smaller businesses: enzymes, APIs, and environmental solutions. Together, they tell the story of a company trying to balance legacy leadership with future bets.

| Segment | FY25 (₹ Cr) | % FY25 | Q1 FY26 (₹ Cr) | % Q1 FY26 | Commentary |

|---|---|---|---|---|---|

| Nutrition (Vitamin D₃ & related) | 350 | 73% | 114.6 | 79% | Continues to dominate; driven by Human & Animal Nutrition growth. |

| Other Business (APIs, Enzymes, Environmental) | 67 | 14% | 18.3 | 13% | APIs slightly weaker QoQ; Environmental Solutions strong triple-digit growth. |

| Value Unlocking (Real Estate) | 45 | 9% | 1.6 | 1% | Non-core; Q1 had one-off land sale. |

| Other Income | 19 | 4% | 12.0 | 8% | Includes forex gain, rental income. |

| Total | 481 | 100% | 144.9 | 100% | YoY growth intact, mix broadly stable. |

Even in the latest quarter, Nutrition continues to contribute \~80% of revenue. Other businesses are growing, but the core thesis remains Vitamin D₃-centric.

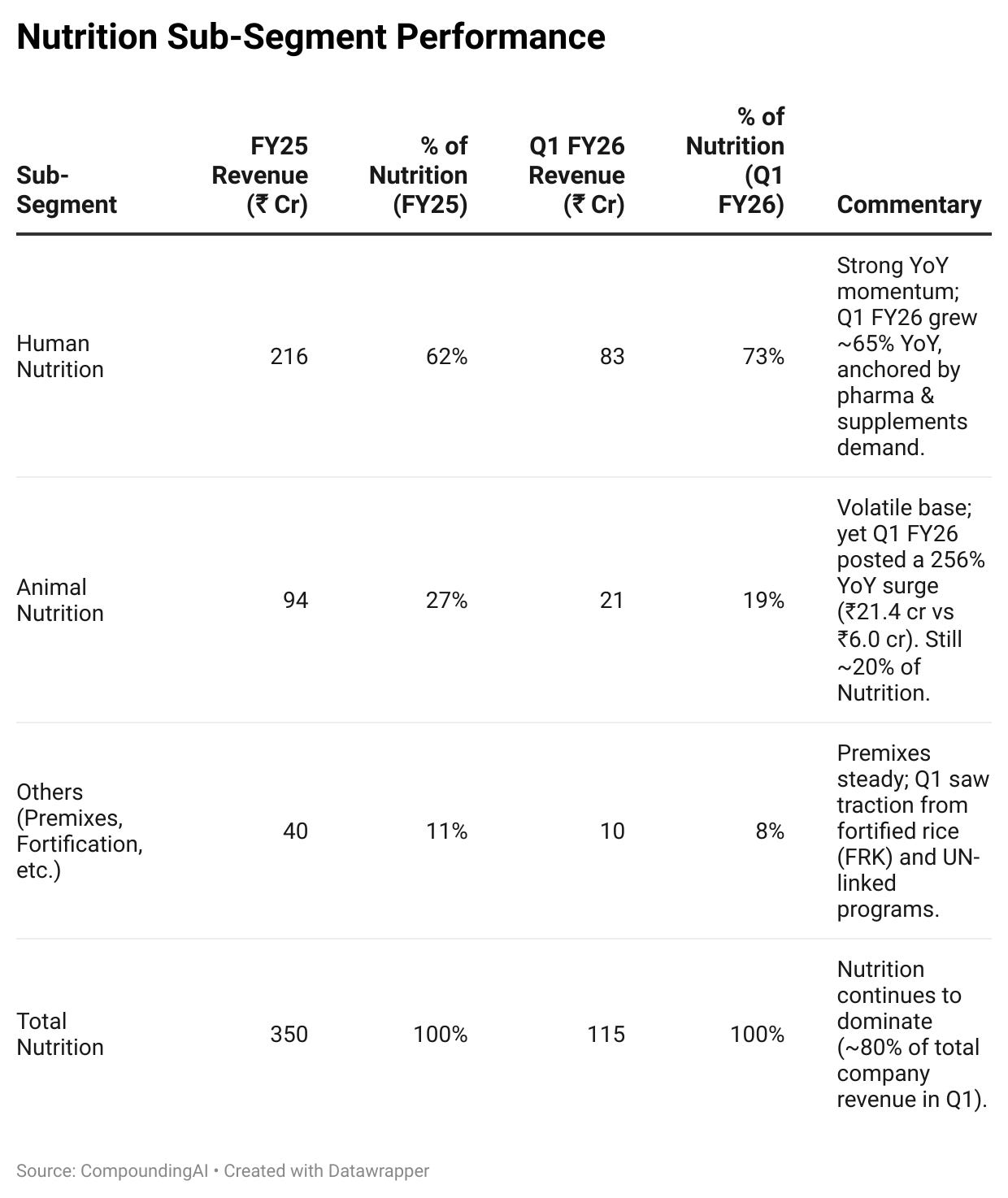

2. Vitamin D₃: The Crown Jewel

Fermenta is the sole manufacturer of Vitamin D₃ in India and ranks among the top three globally. This position is no accident, it stems from over 55 years of manufacturing expertise, backward integration into cholesterol (a key raw material), and a supply chain deliberately structured to be non-China dependent.

Breakdown of Nutrition (FY25)

| Sub-Segment | Revenue (₹ Cr) | % of Nutrition |

|---|---|---|

| Human Nutrition | 216 | 62% |

| Animal Nutrition | 94 | 27% |

| Others (Premixes, Fortification, etc.) | 40 | 11% |

| Total Nutrition | 350 | 100% |

{kind=link}

- Human Nutrition is consolidating its role as the anchor, now nearly three-fourths of the Nutrition mix.

- Animal Nutrition remains lumpy but is bouncing hard off a low base, with triple-digit YoY growth in Q1 FY26.

- Premixes & Fortification are smaller, but strategically important given GAIN/WFP approvals expect this line to matter more from FY27 onwards.

- Overall, Q1 FY26 shows that the Nutrition segment isn’t just stable, it’s expanding faster than the rest of the portfolio, reinforcing Fermenta’s D₃-centric moat.

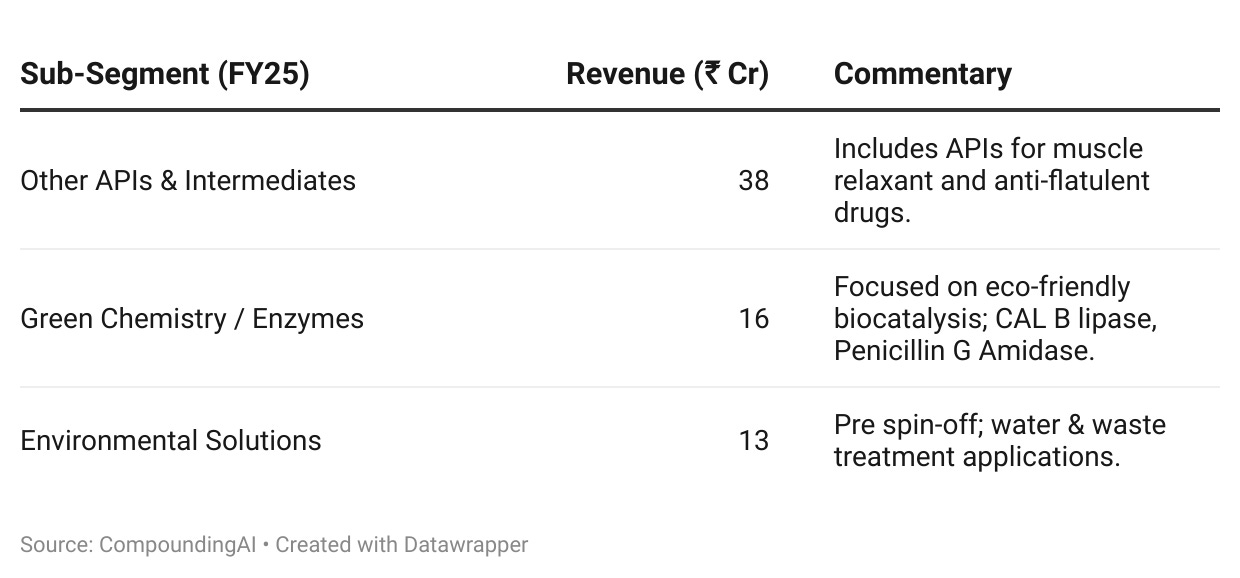

3. Enzymes, APIs, and Green Chemistry: The Diversifiers

| Sub-Segment (FY25) | Revenue (₹ Cr) | Commentary |

|---|---|---|

| Other APIs & Intermediates | 38 | Includes APIs for muscle relaxant and anti-flatulent drugs. |

| Green Chemistry / Enzymes | 16 | Focused on eco-friendly biocatalysis; CAL B lipase, Penicillin G Amidase. |

| Environmental Solutions | 13 | Pre spin-off; water & waste treatment applications. |

{kind=link}

Takeaway: APIs and enzymes provide technical credibility. Fermenta was among the first to commercialize immobilized enzymes in India and continues to push lipases for niche applications.

But growth has been uneven APIs spiked in certain quarters (Q3 FY25 saw a 7500% jump off a low base), while enzymes are steady but not transformational. Environmental Solutions has now been spun out more on that later.

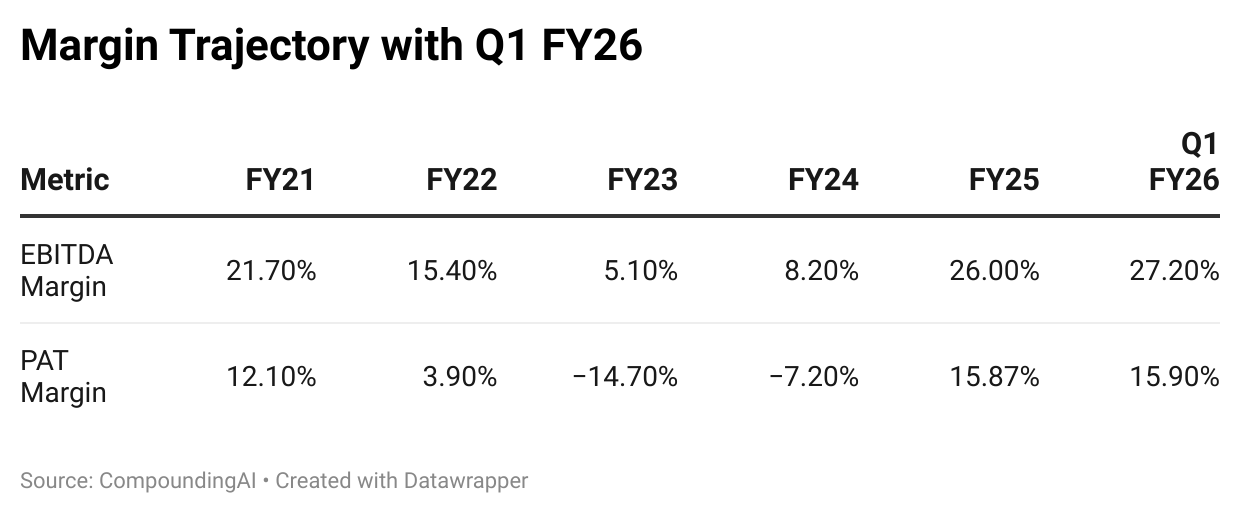

4. Margins: From Collapse to Comeback

Perhaps the most dramatic part of Fermenta’s story is its margin rollercoaster.

| Metric | FY21 | FY22 | FY23 | FY24 | 9M FY25 | Q1 FY26 |

|---|---|---|---|---|---|---|

| EBITDA Margin | 21.7% | 15.4% | 5.1% | 8.2% | 22.1% | 27.2% |

| PAT Margin | 12.1% | 3.9% | -14.7% | -7.2% | 13.1% | 15.9% |

{kind=link}

Timeline of Turnaround:

- FY21: Strong base year.

- FY22–23: Collapse : animal feed volatility, under-absorption of costs, exceptional losses. PAT went deep red.

- FY24: Green shoots, but PAT still negative.

- FY25: Revival : raw material costs down, debt cut, margins bounce back.

- Q1 FY26: Highest EBITDA margin in five years at 27.2%, showing the turnaround is sticking.

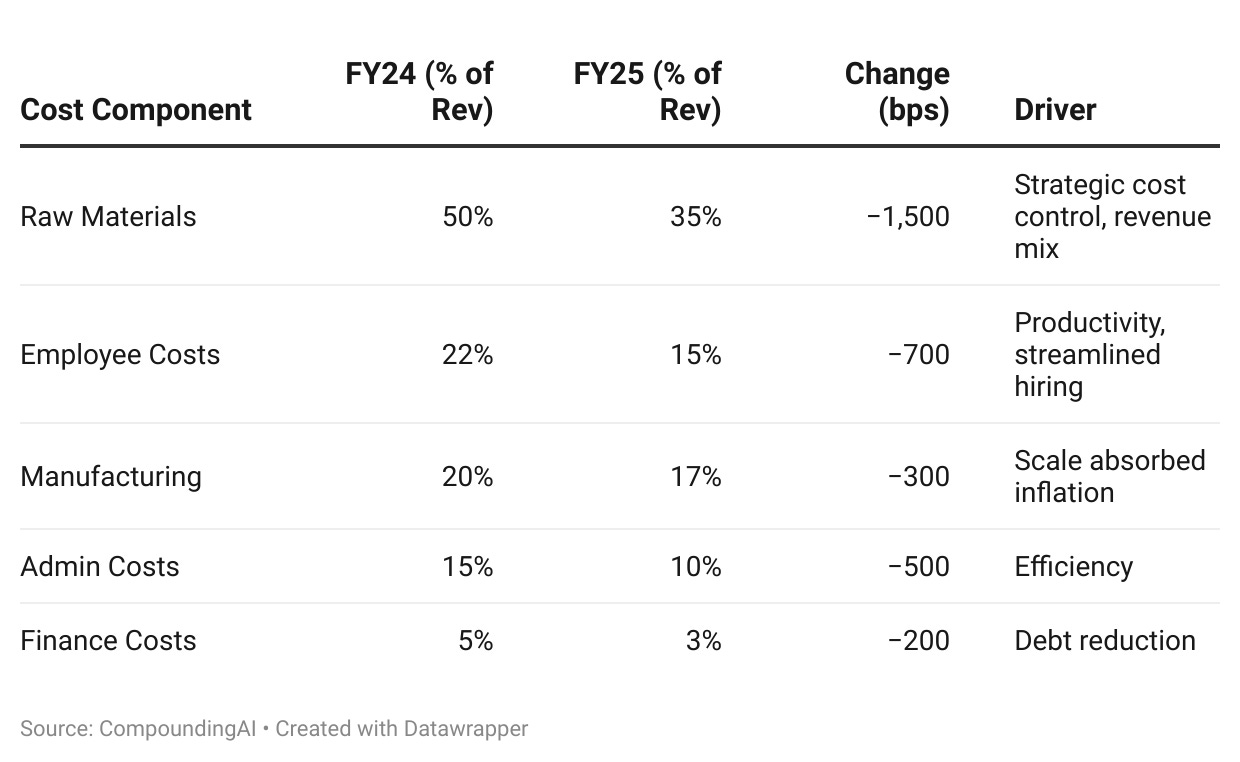

5. Cost Discipline

{kind=link}

Fermenta didn’t just get lucky with markets, it cut deep into every cost line, laying the foundation for sustained profitability.

| Cost Component | FY24 (% of Rev) | FY25 (% of Rev) | Change (bps) | Driver |

|---|---|---|---|---|

| Raw Materials | 50% | 35% | -1500 | Strategic cost control, revenue mix |

| Employee Costs | 22% | 15% | -700 | Productivity, streamlined hiring |

| Manufacturing | 20% | 17% | -300 | Scale absorbed inflation |

| Admin Costs | 15% | 10% | -500 | Efficiency |

| Finance Costs | 5% | 3% | -200 | Debt reduction |

6. Supply Chain Resilience

Fermenta’s supply chain is central to its moat.

- Backward Integration: Cholesterol sourced from sheep wool, reducing reliance on external suppliers.

- Plant-Based D₃: Patent-protected phytosterol route (VITADEE™ Green™) adds a vegan, sustainable option.

- Non-China Dependent: Unlike many peers, Fermenta built resilience outside China, critical during supply shocks.

- FX Exposure: With \~60% of revenue overseas, currency swings matter. A stronger rupee hurts margins, but global certifications (FDA, CEP, WHO GMP, FAMI-QS) act as passports to ensure access to premium markets.

7. Segmental and Operational Analysis

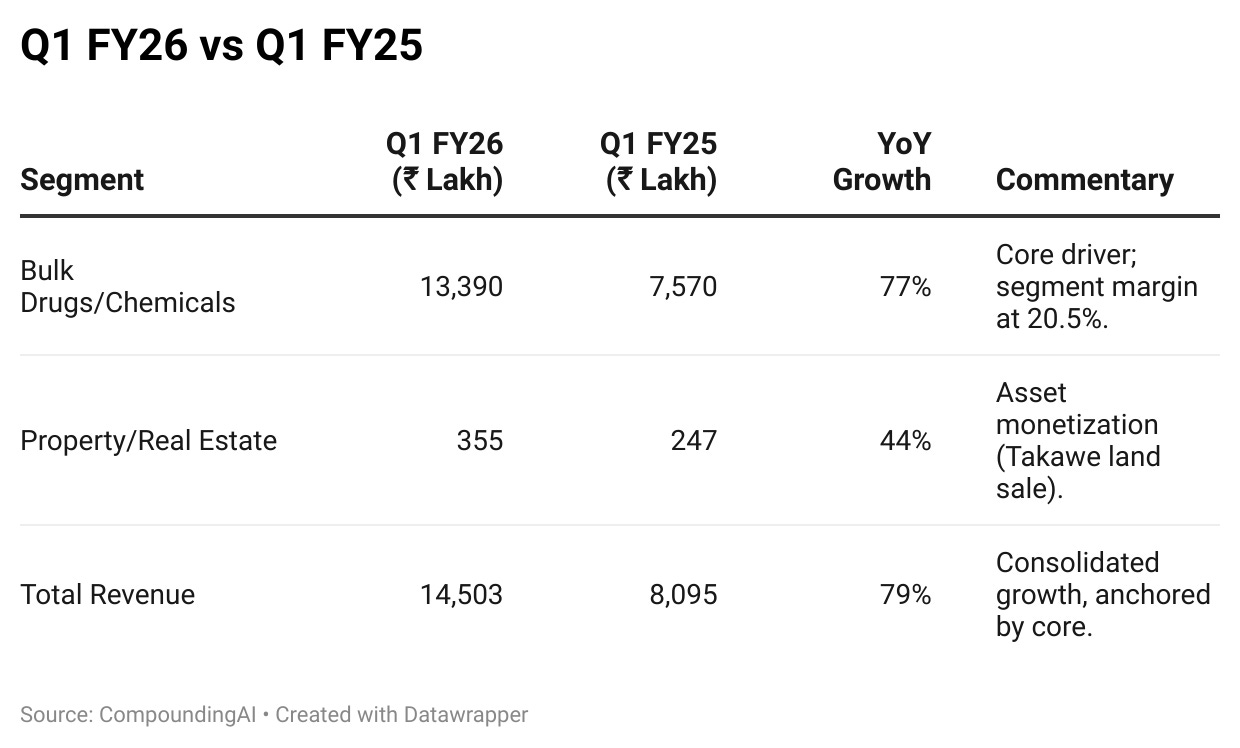

Q1 FY26 vs Q1 FY25

{kind=link}

| Segment | Q1 FY26 (₹ Lakh) | Q1 FY25 (₹ Lakh) | YoY Growth | Commentary |

|---|---|---|---|---|

| Bulk Drugs/Chemicals | 13,389.9 | 7,569.7 | +77.0% | Core driver; segment margin at 20.5%. |

| Property/Real Estate | 355.2 | 247.0 | +43.8% | Asset monetization (Takawe land sale). |

| Total Revenue | 14,503.4 | 8,095.0 | +79.2% | Consolidated growth, anchored by core. |

Even excluding property sales, core revenue surged >70% YoY.

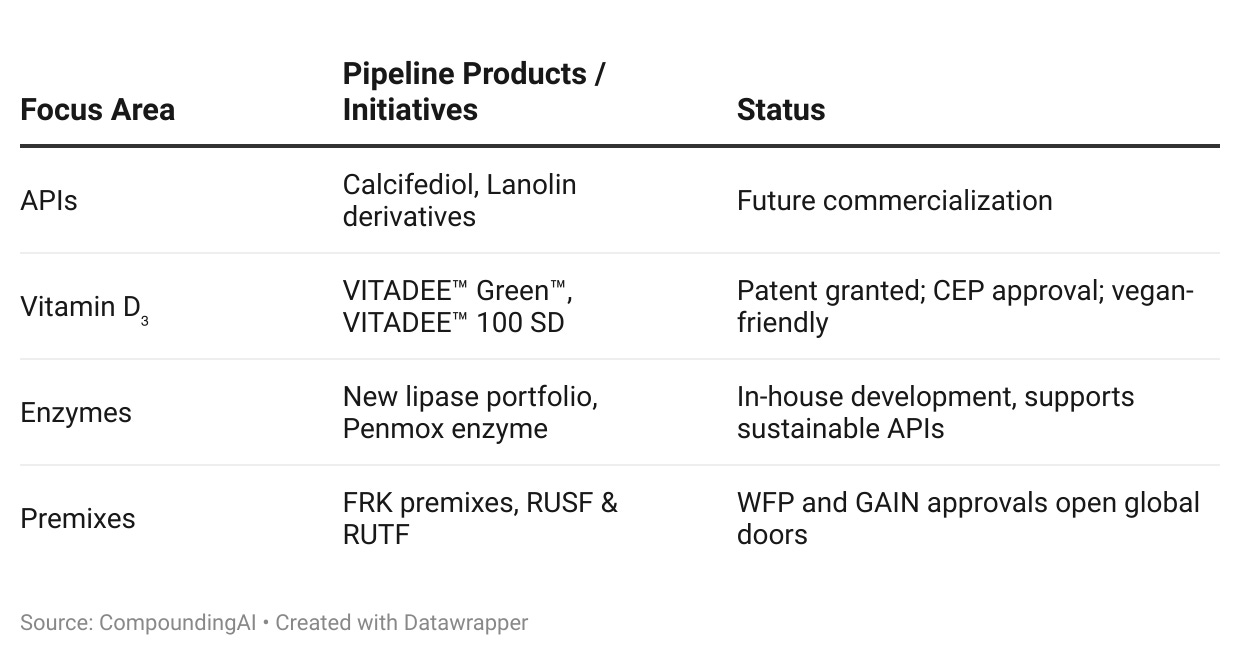

8. R\&D and the Pipeline

Fermenta isn’t just riding Vitamin D₃; it’s investing in new molecules.

| Focus Area | Pipeline Products / Initiatives | Status | Strategic Significance |

|---|---|---|---|

| APIs | Calcifediol, Lanolin derivatives | Future commercialization | Expands Vitamin D family; potential new revenue stream in cosmetics & nutraceuticals. |

| Vitamin D₃ | VITADEE™ Green™, VITADEE™ 100 SD | Patent granted; CEP approval; vegan-friendly | Vegan market growth + regulatory credibility in Europe. |

| Enzymes | New lipase portfolio, Penmox enzyme | In-house development | Positions Fermenta as a biocatalysis supplier in green chemistry. |

| Premixes | FRK premixes, RUSF & RUTF | WFP and GAIN approvals | Access to UN & global nutrition programs. |

{kind=link}

This R\&D pipeline is both a hedge and an opportunity, diversification that may reduce over-reliance on Vitamin D₃ over time.

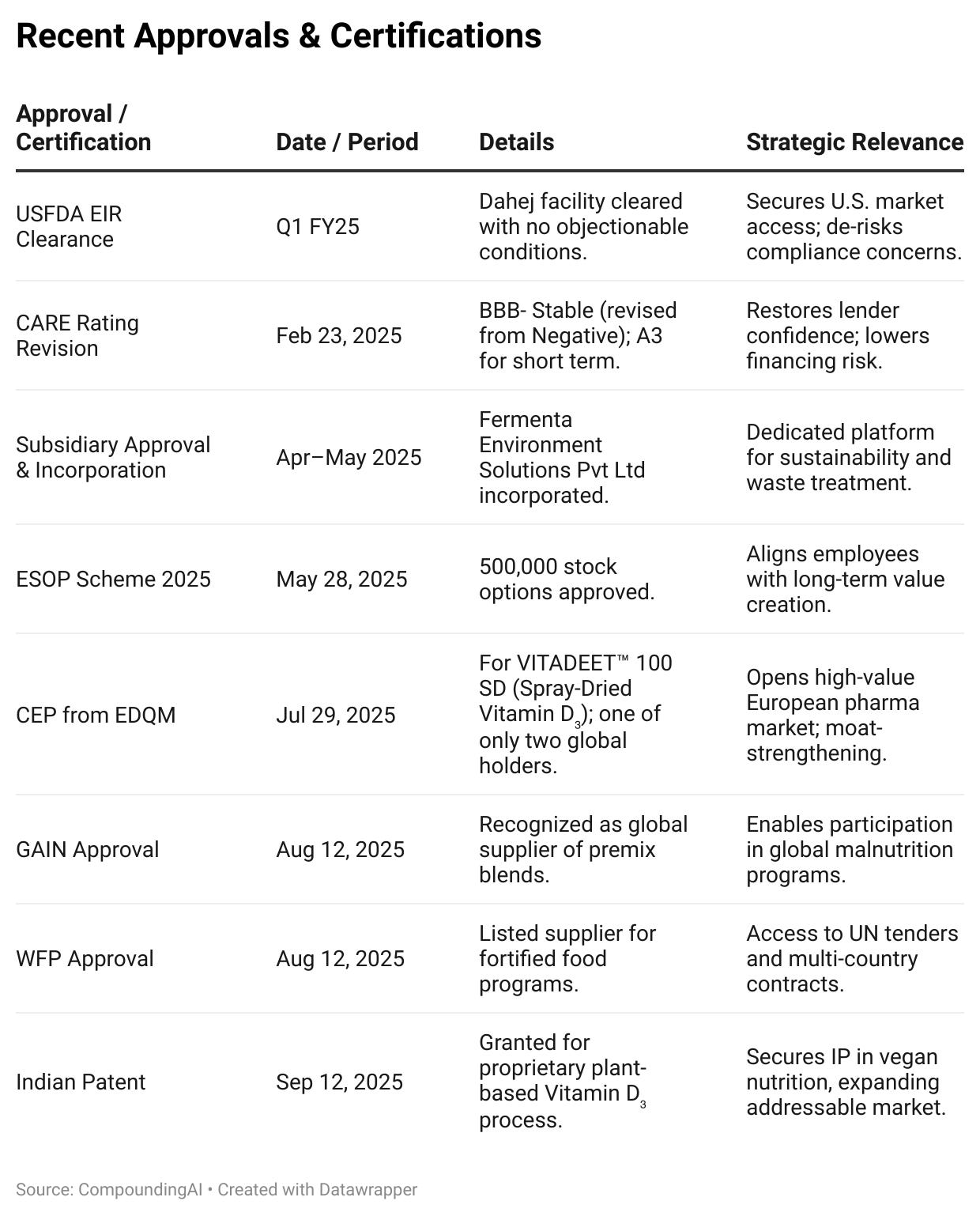

9. Recent Approvals: Building Global Trust

In the world of specialty molecules, a certificate can be as valuable as a factory. Without regulatory blessings, even the best chemistry sits idle. Fermenta knows this well and in the past 18 months, it has stitched together a string of critical approvals that strengthen both its moat and its credibility.

Recent Approvals & Certifications

| Approval / Certification | Date / Period | Details | Strategic Relevance |

|---|---|---|---|

| USFDA EIR Clearance | Q1 FY25 | Dahej facility cleared with no objectionable conditions. | Secures U.S. market access; de-risks compliance concerns. |

| CARE Rating Revision | Feb 23, 2025 | BBB- Stable (revised from Negative); A3 for short term. | Restores lender confidence; lowers financing risk. |

| Subsidiary Approval & Incorporation | Apr–May 2025 | Fermenta Environment Solutions Pvt Ltd incorporated. | Dedicated platform for sustainability and waste treatment. |

| ESOP Scheme 2025 | May 28, 2025 | 500,000 stock options approved. | Aligns employees with long-term value creation. |

| CEP from EDQM | Jul 29, 2025 | For VITADEET™ 100 SD (Spray-Dried Vitamin D₃); one of only two global holders. | Opens high-value European pharma market; moat-strengthening. |

| GAIN Approval | Aug 12, 2025 | Recognized as global supplier of premix blends. | Enables participation in global malnutrition programs. |

| WFP Approval | Aug 12, 2025 | Listed supplier for fortified food programs. | Access to UN tenders and multi-country contracts. |

| Indian Patent | Sep 12, 2025 | Granted for proprietary plant-based Vitamin D₃ process. | Secures IP in vegan nutrition, expanding addressable market. |

{kind=link}

Commentary:

This isn’t just alphabet soup. Each approval functions as a “passport” to markets or segments otherwise closed. FDA and CEP open regulated geographies; GAIN and WFP plug Fermenta into global food security chains; the patent on plant-based D₃ gives defensibility in a growing niche.

Together, they turn Fermenta from a niche supplier into a globally recognized, audit-ready player.

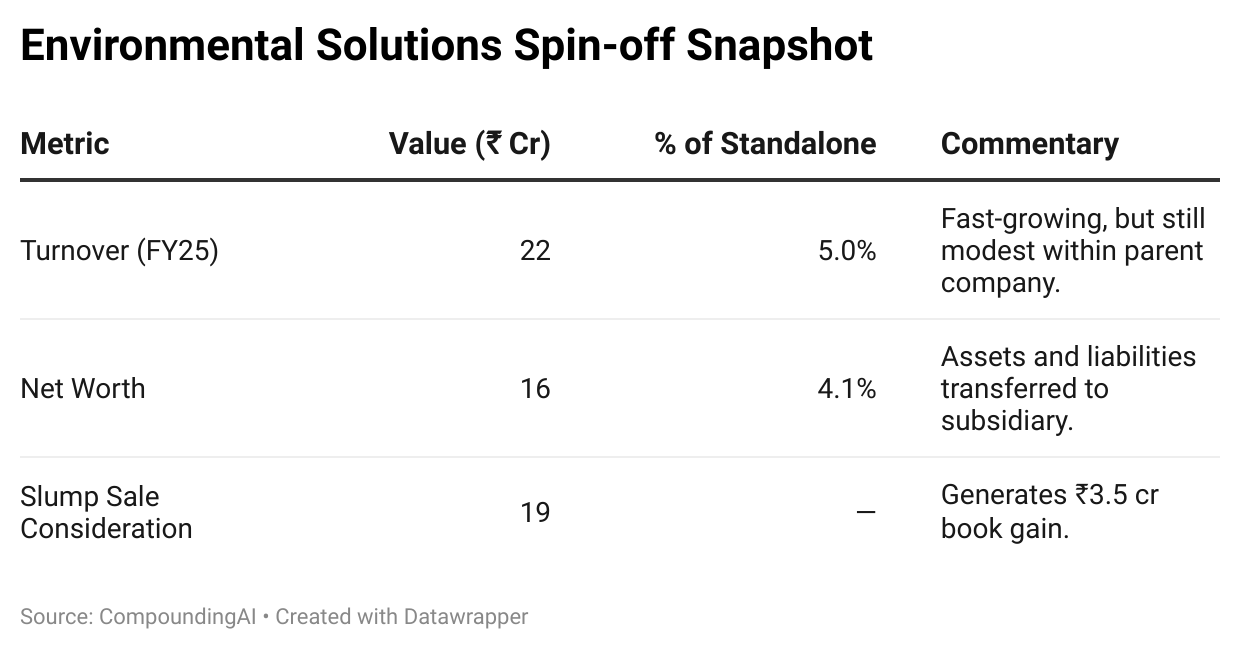

10. Environmental Solutions Spin-off

For years, Environmental Solutions was a side business - small in scale, but aligned with the sustainability zeitgeist.

In September 2025, Fermenta hived it off into a wholly owned subsidiary, Fermenta Environment Solutions Pvt Ltd (FESPL), through a slump sale.

Environmental Solutions Spin-off Snapshot

| Metric | Value (₹ Cr) | % of Standalone | Commentary |

|---|---|---|---|

| Turnover (FY25) | 22.20 | 5.0% | Fast-growing, but still modest within parent company. |

| Net Worth | 15.53 | 4.1% | Assets and liabilities transferred to subsidiary. |

| Slump Sale Consideration | 19.00 | — | Generates ₹3.5 cr book gain. |

{kind=link}

Takeaway:

The move does three things at once:

- Financial Focus – Parent sharpens capital allocation on Nutrition and APIs.

- Strategic Clarity – Environmental solutions (water treatment, bioremediation, waste management) now gets its own management bandwidth.

- Value Unlocking – Given the segment grew >200% YoY in recent quarters, the spin-off sets it up to attract its own partnerships, perhaps even external capital, without diluting Fermenta’s focus.

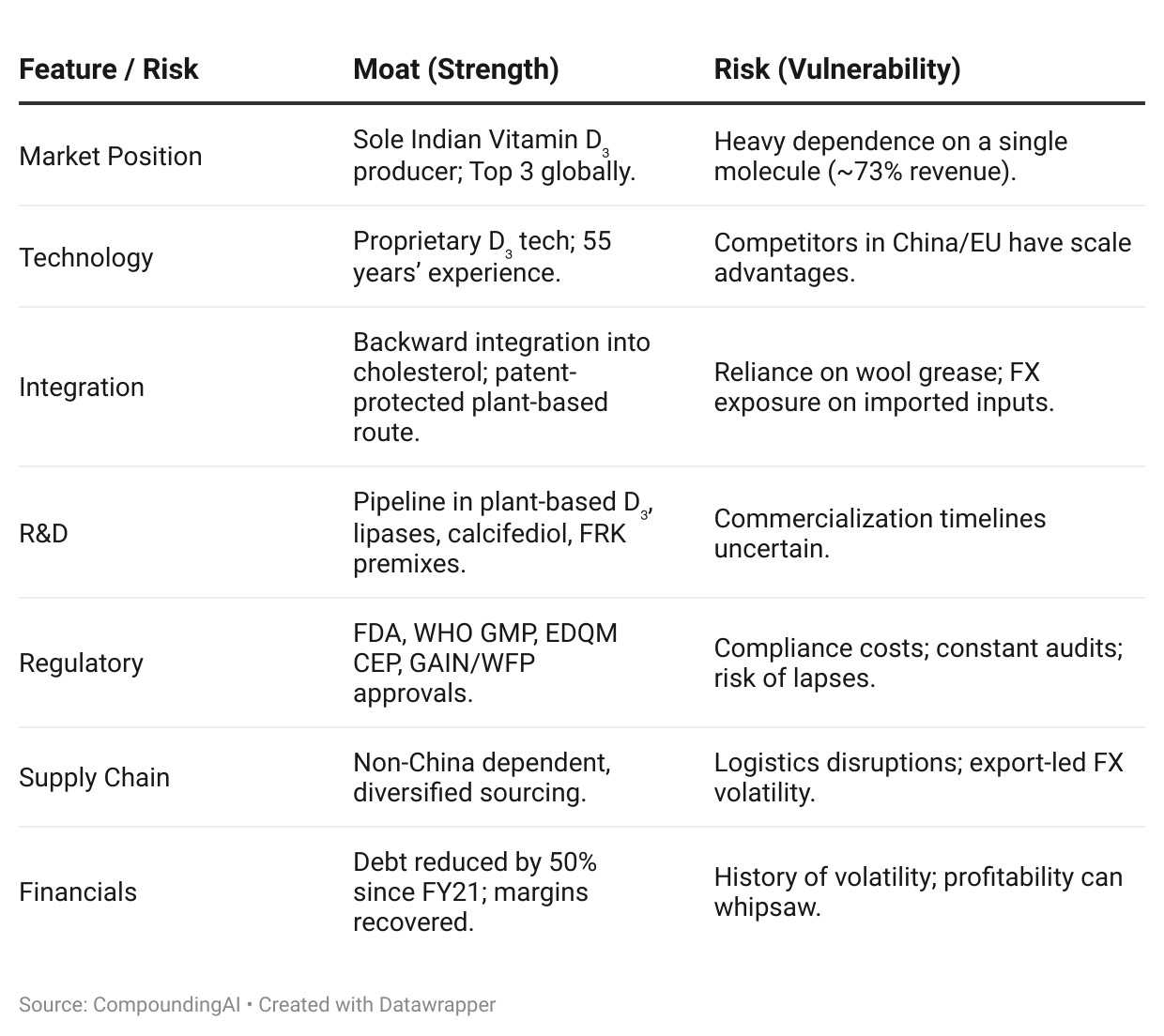

11. Moats vs Risks

Fermenta’s story is equal parts strength and vulnerability. The tables tell it best.

| Feature / Risk | Moat (Strength) | Risk (Vulnerability) |

|---|---|---|

| Market Position | Sole Indian Vitamin D₃ producer; Top 3 globally. | Heavy dependence on a single molecule (\~73% revenue). |

| Technology | Proprietary D₃ tech; 55 years’ experience. | Competitors in China/EU have scale advantages. |

| Integration | Backward integration into cholesterol; patent-protected plant-based route. | Reliance on wool grease; FX exposure on imported inputs. |

| R\&D | Pipeline in plant-based D₃, lipases, calcifediol, FRK premixes. | Commercialization timelines uncertain. |

| Regulatory | FDA, WHO GMP, EDQM CEP, GAIN/WFP approvals. | Compliance costs; constant audits; risk of lapses. |

| Supply Chain | Non-China dependent, diversified sourcing. | Logistics disruptions; export-led FX volatility. |

| Financials | Debt reduced by 50% since FY21; margins recovered. | History of volatility; profitability can whipsaw. |

{kind=link}

Takeaway: The moat is real, but so is concentration risk. Fermenta’s challenge is to keep expanding the pie, so that D₃ remains the anchor, not the entire ship.

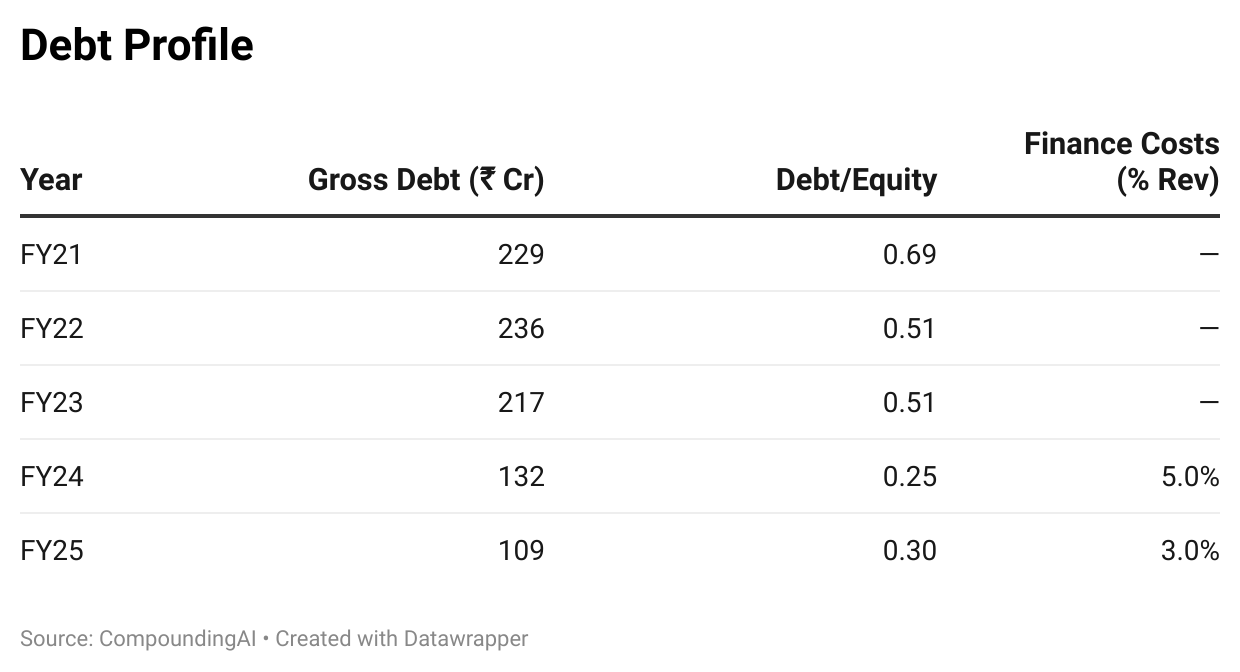

12. Debt and Balance Sheet Discipline

A decade ago, Fermenta might have been written off as debt-burdened and margin-weak. But FY25 proved it could clean up.

Debt Profile

| Year | Gross Debt (₹ Cr) | Debt/Equity | Finance Costs (% Rev) |

|---|---|---|---|

| FY21 | 229 | 0.69 | — |

| FY22 | 236 | 0.51 | — |

| FY23 | 217 | 0.51 | — |

| FY24 | 132 | 0.25 | 5% |

| FY25 | 109 | 0.30 | 3% |

{kind=link}

Commentary:

- Gross debt halved in four years.

- Finance costs fell to just 3% of revenue.

- Liquidity ratios (current ratio 1.52, quick ratio 0.87) suggest headroom.

This cleanup was survival. Without it, the margin recovery in FY25 would have been eaten up by interest expense. The company is now in a position to fund R\&D and scale new segments without overleveraging.

13. Currency & Trade Risks

Fermenta’s international footprint is both its moat and its Achilles’ heel.

- 60% revenue outside India – Exposure is structural, not tactical.

- Geography Mix (9M FY25): India 40%, Europe 26%, North America 17%, Others 17%.

- FX Swings: A stronger rupee compresses margins; volatility in EUR and USD matter most.

- Trade Barriers: Mitigated by certifications (FDA, EDQM, WHO GMP, FAMI-QS, GAIN/WFP). These act as “passports” that lower the friction of exporting across 60+ countries.

- Cost of Compliance: The price of these passports is recurring audits, staff overheads, and regulatory upkeep.

In short: Fermenta’s global reach gives it pricing power, but the FX and regulatory grind is the hidden tax it must keep paying.

14. Pulling It Together: What to Watch

Fermenta is a company in motion, rebuilding its moat while diversifying its risks. For investors and observers, three signals will decide whether the turnaround sticks.

- Vitamin D₃ stability – Human and animal nutrition volumes must sustain double-digit growth. D₃ is still the anchor.

- R\&D commercialization – Plant-based D₃ and premixes must move from lab to revenue. Without this, diversification remains theoretical.

- Margin discipline – The cost reset of FY25 must persist, even if feed prices swing again.

Closing Thoughts

Fermenta Biotech is not a household name. But in the world of molecules that invisibly shape our food, health, and environment, it is a quiet giant.

The comeback in FY25 was remarkable. The continuation in Q1 FY26 with revenue up 74%, EBITDA margin at 27%, and PAT margin at 16% makes it real.

The moat is real but so are the risks. For investors and industry watchers alike, Fermenta is a lesson in how even the most specialized companies must constantly evolve their portfolio, balance sheet, and strategy to stay relevant.

This piece is created using inputs only from CompoundingAI.

CompoundingAI is an enterprise-grade vertical intelligence engine that transforms unstructured corporate filings into decision-grade insights within minutes, complete with source-level traceability for confident, auditable workflows.

We cut the noise & directly deliver insights.

Note : Not a buy/sell recommendation. For education purpose only.

Powered by CompoundingAI — AI research platform for Indian stocks, every claim cited from primary filings

Login Now