KRN Heat Exchanger and Refrigeration Ltd. FY25 Results: Revenue Beat, Margin Recovery, and a 1000 Cr Vision I CompoundingAI

KRN Q4 FY25 Results: Revenue Beats, Margin Recovery, Expansion in Play

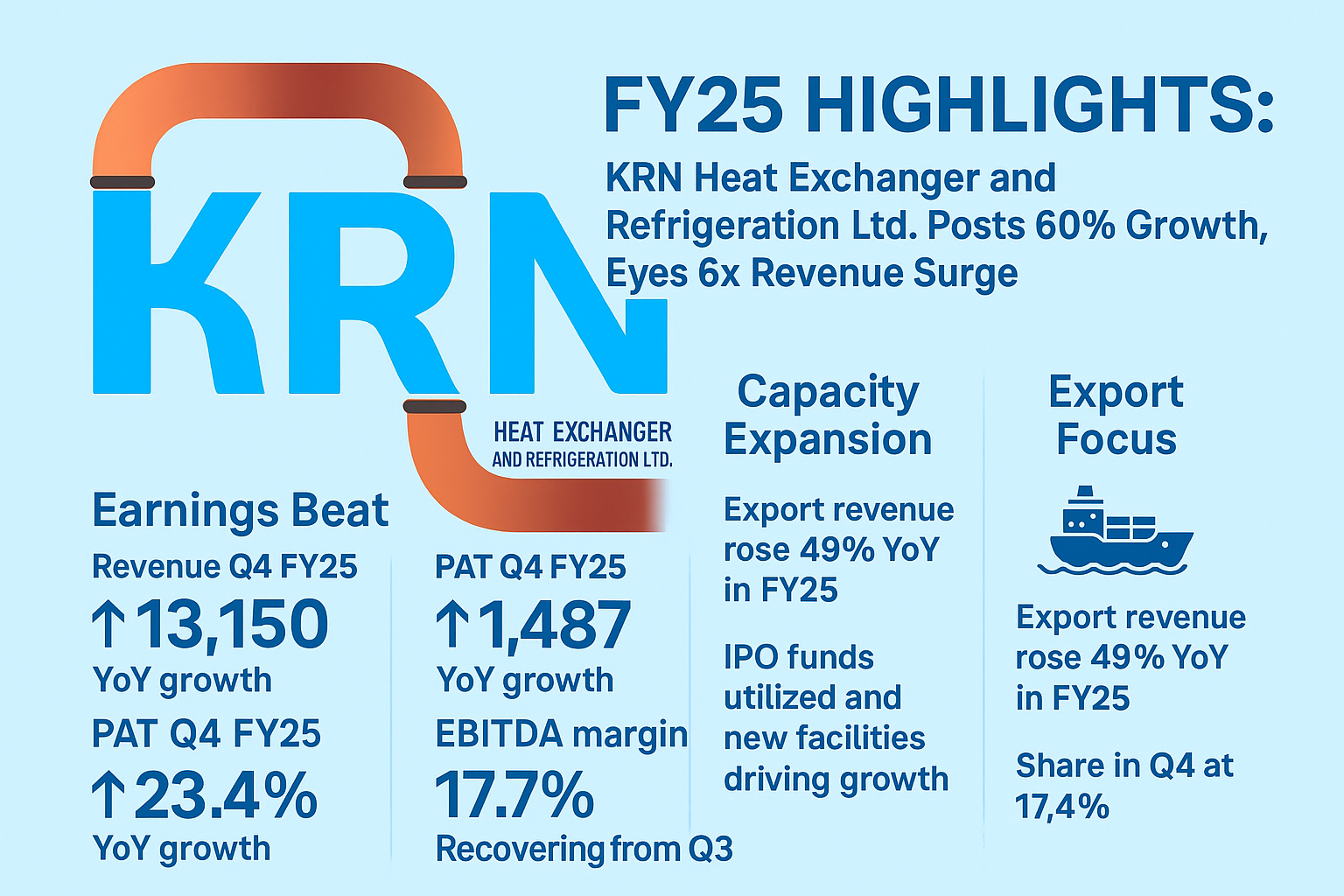

KRN posts 60% YoY revenue growth in Q4 FY25, beating guidance. Margin recovery, strong exports, and capacity expansion underscore long-term potential.

When a manufacturing company surpasses expectations during a pivotal capacity expansion phase, it sends a strong signal to the market about its execution capability and long-term roadmap. That’s precisely the story of KRN Heat Exchanger and Refrigeration Ltd. in FY25.

The company not only beat its own revenue guidance in Q4 but also improved full-year margins, advanced its strategic expansion, and made material progress in exports and subsidiary performance.

Q4 FY25: Exceeding Expectations

KRN reported consolidated revenue from operations of ₹131.5 Cr in Q4 FY25, reflecting a 60.4% YoY and 18% QoQ increase. This strong beat over management’s own guidance (0-10% QoQ growth) suggests accelerating order momentum and successful execution.

- PAT rose to ₹14.87 Cr, up 23.4% YoY.

- EBITDA climbed to ₹23.22 Cr, a 20.5% YoY increase.

- EBITDA margin stood at 17.66%, up from \~14.18% in Q3 but lower than 23.5% in Q4 FY24.

- EPS (Basic/Diluted): ₹2.39 vs ₹2.12 in Q3 and ₹2.62 in Q4 FY24.

What drove this beat?

- Export revenue acceleration (+68.4% QoQ).

- New customer additions from North America and Europe.

- Partial cost pass-through post January 1st.

- Initial revenue from KRN HVAC subsidiary (expansion-linked entity).

However, YoY margin compression reflects high employee onboarding and preparatory costs for the new facility, echoing Q3 management commentary.

FY25 Annual Performance: Scaling Without Slipping

Full-year revenue surged 39.4% YoY to ₹429.8 Cr, with PAT growing 34.2% to ₹52.88 Cr. Importantly, the EBITDA margin improved to 19.16% from 18.96%, reflecting strong control even amid expansion overheads.

Other full-year highlights:

- PBT: ₹74.32 Cr, up 32.9% YoY

- EPS: ₹9.75 vs ₹8.76 in FY24

- Total Income: ₹441.7 Cr, +40.8% YoY

Margins were bolstered by improved scale, operating leverage in existing facilities, and growing contribution from high-margin export orders.

Export Traction: Taking the Global Route

KRN’s international strategy began to bear fruit in FY25:

- FY25 export revenue: ₹67.45 Cr, up 49% YoY.

- Q4 export share: 17.4% of revenue (vs 12.2% in Q3).

Key drivers:

- "China plus one" sourcing shift.

- Anti-dumping duties against competitors in North America.

- Entry into new markets like UAE and Canada.

With management targeting 50% export revenue in the long term, FY25’s traction validates their global pivot.

Capacity Expansion: Foundation for 6x Growth

KRN is executing a ₹235.8 Cr capex plan via its subsidiary KRN HVAC Products Pvt. Ltd. in Neemrana. Evidence of progress:

- CWIP: ₹82.27 Cr (up 17x YoY)

- PPE: ₹85.2 Cr (up ₹33.4 Cr YoY)

- IPO proceeds: Fully utilized as per prospectus

The new facility is slated to begin sampling in April 2025 and mass production in H2 FY26. It’s designed to increase peak revenue 5–6x over 3 years.

Even before full commissioning, the subsidiary clocked ₹15.5 Cr revenue and ₹2.78 Cr PAT in FY25 , a healthy early signal.

Margin Watch: Investments Now, Returns Later

The drop in Q4 FY25 margin (YoY) isn’t unexpected. Management had flagged:

- Higher employee costs (150+ hires under training)

- Opex for new facility readiness

- Volatile raw material prices

That said, sequential margin recovery (from Q3 to Q4) and full-year margin improvement suggest costs are being absorbed in stride.

The target? A 1-2% gross margin uptick once ramp-up stabilizes.

R\&D Bet: Thermotech Research Lab

KRN also set up Thermotech Research Laboratory Pvt. Ltd. to lead HVAC-specific R\&D, quality testing, and technical certifications. Though it posted a minor loss of ₹8.16 Lakhs and zero revenue in FY25, it is strategically important for:

- Global certifications for exports

- HVAC lab testing infrastructure

- Product innovation and customization

Balance Sheet Health: Powered by IPO

- Equity base: ₹498.6 Cr (up from ₹130.3 Cr)

- Debt: Reduced across both short and long term

- Cash & equivalents: ₹102.6 Cr

- Other Bank Balances: ₹140.9 Cr (likely IPO funds held temporarily)

The IPO clearly strengthened the balance sheet, giving KRN dry powder to execute capex without overleveraging.

Cash Flows: Investing in Growth

- Operating cash flow: ₹21.4 Cr, up from ₹16.9 Cr

- Capex outflow: ₹78.8 Cr in CWIP investments

- Net financing inflow: ₹257.8 Cr (IPO-led)

KRN managed to improve cash generation from core operations even while absorbing heavy expansion costs.

Key Questions Ahead

- Can KRN ramp up exports toward its >50% target?

- How soon can bar & plate and roll-bond products scale?

- Will the new plant meet its H2 FY26 production schedule?

- Is margin guidance (1-2% improvement) achievable in FY26?

Final Take: Ready for the Next Leap

FY25 marks the end of one chapter for KRN and the start of another. The company has proven its ability to scale, absorb costs, and build strategically. With IPO funds deployed, capacity in place, and global orders kicking in, the next two years will determine whether KRN transitions from a fast-growing mid-cap to a global-scale manufacturing player.

Looking to decode earnings with real context and signals?

CompoundingAI helps investors and analysts surface critical trends, margin drivers, and competitive positioning instantly from filings, calls, and financials across 1800+ Indian companies.

Powered by CompoundingAI — AI research platform for Indian stocks, every claim cited from primary filings

Login Now