The Chemistry of Redemption: Meghmani Organics and the Mid-Cap Chemicals Credibility Cycle

Indian chemical companies don’t just run on feedstock and demand cycles. They also run on credibility cycles.

First comes promise, bold capex announcements and ambitious revenue targets. Then bust, underdelivery and eroded trust. The few survivors relearn candor in the repair phase. And only the disciplined reach the reward phase, where the market re-rates them as compounders.

Meghmani Organics Ltd. (MOL), long stuck in the bust, is now tentatively entering repair. The question is whether it can follow the path of Aarti and Atul or end up like peers who never escaped the penalty box.

I. Broken Promises: Why Guidance Matters More Than Growth

Every investor has scars from companies that overpromised and underdelivered. For followers of Meghmani Organics Ltd. (MOL), that scar tissue runs deep.

The company once dangled visions of revenue doubling and margin expansion. Instead, FY24 became a graveyard of those promises: stalled revenues, underutilized plants, receivables spiraling upward, and subsidiaries draining capital.

It was a credibility collapse.

But chemical companies, like their products, are cyclical. They are shaped by capex curves, regulatory moods, global demand shifts, and internal discipline. The story of MOL post-FY25 is one of cautious redemption, not yet complete, but perhaps on a trajectory few would have believed two years ago.

II. Relearning the Art of Guidance

Guidance is the social contract between management and investors.

- MOL in FY24: Big proclamations, little delivery. Guidance was linear, grand, and detached from operating realities.

- MOL in FY26: More segmented, tied to product cycles, explicit about risks (e.g., anti-dumping duty expiry for TiO₂, adoption lags for nano urea).

This shift mirrors what Aarti Industries did in FY18–20. After a period of stretched promises and opaque disclosures, Aarti recalibrated, moved to order-book-based guidance, and gradually rebuilt trust. Investors re-rated the stock only after three years of consistent adherence.

💡 Sidebar: What Aarti Did Right in 2018

- Cut down “headline” guidance, moved to segmental order-book commentary.

- Focused on utilization metrics, not revenue dreams.

- Shared risks upfront (raw material volatility, regulatory approvals).

- By FY21, trust rebuilt → valuations expanded.

III. When Unit Economics Heal

Topline numbers deceive; margins per unit tell the truth.

MOL’s FY24–25 transition is best seen in EBITDA/tonne:

| Segment | FY24 EBITDA/tonne | FY25 EBITDA/tonne | % Change |

|---|---|---|---|

| Crop Protection | ₹11,990 | ₹42,308 | +253% |

| Pigments | –₹4,810 | ₹17,654 | Turned Positive |

This echoes Atul Ltd., which has built its reputation by talking less about growth percentages and more about return on capital employed (ROCE), margins per business line, and cash generation. Atul rarely excites with guidance but impresses with consistency.

MOL is not Atul yet. But the per-tonne turnaround, especially in pigments,the kind of micro-improvement Atul’s long-term investors look for before believing a turnaround.

💡 Sidebar: Atul’s Secret Weapon - ROCE First, Growth Second

Atul’s management repeatedly emphasizes that growth without ROCE is hollow.

In downturns, they scale down production rather than chase volumes at negative spreads. This discipline has earned them a “premium multiple for boredom.”

IV. Management Candor: The Most Underpriced Asset

Markets forgive volatility, never opacity.

MOL’s Q1 FY26 concall sounded different from FY24’s evasions. Kapil Garg openly admitted:

- ONGC holiday orders are seasonal.

- Subsidiaries remain margin-dilutive.

- TiO₂ is government-policy dependent.

This candor is reminiscent of Navin Fluorine in FY21–22, when it over-communicated every risk around the Dahej plant capex, including raw material volatility. Investors rewarded that transparency with premium multiples.

Ironically, Navin’s more recent stumbles (delays in new fluorochemicals ramp-up, abrupt management exits) show what happens when candor disappears again.

💡 Sidebar: How Navin Lost Trust in 2023

- FY21–22: Navin was the darling of the specialty chemical boom.

- FY23: Delayed Dahej project, poor disclosures on capex overruns.

- FY24: Sudden leadership churn, guidance cuts.

- Market response: P/E de-rated from 45× to \~25× in under 18 months.

V. Capital Allocation: Sweating Old Capex

The question for MOL isn’t what new projects it will announce. It’s whether its ₹1,150 crore capex over FY22–24 will sweat.

| Project | Investment (₹ cr) | Potential Impact | Key Risk |

|---|---|---|---|

| Multi-Purpose Plant | 500–600 | Up to ₹1,000 cr revenue by FY28 | Utilization risk |

| Nano Urea | 250 | Policy-aligned agri optionality | Farmer adoption lag |

| TiO₂ | 300 | Import substitution opportunity | ADD expiry risk |

Compare this with Aarti Industries’ toluene chain expansions (FY16–20) or Atul’s integrated aromatics investments. Both companies sweated their assets ruthlessly, even in downcycles, because management tracked asset utilization like hawks.

If MOL can push utilization >70–80% within 3 years, its capex will compound. If not, it risks becoming another Indian Chemical Story of White Elephants.

VI. Operations & Strategy Execution: Standalone vs. Subsidiary Split

MOL’s standalone business is healthy:

- 48% YoY revenue growth in Q1 FY26.

- Pigments turned profitable.

- Crop protection saw per-tonne margins triple.

But subsidiaries remain the Achilles’ heel: undisciplined, loss-making, margin-dilutive.

Contrast this with Gujarat Fluorochemicals, where group complexity initially depressed valuations until governance clarity improved.

Markets prefer standalone clarity to group complexity. Unless MOL prunes or disciplines subsidiaries, valuation multiples will stay discounted.

VII. Risk Management: From Silence to Acknowledgment

Risks MOL now discloses openly:

- Egypt/Gaza disruptions.

- ADD expiry for TiO₂.

- ONGC contract lumpiness.

This shift matters. A decade ago, Atul Ltd. was one of the few Indian chemical mid-caps to openly admit risks of dependence on China. That honesty built resilience when COVID supply shocks hit.

MOL’s shift to naming risks rather than hiding them signals cultural change.

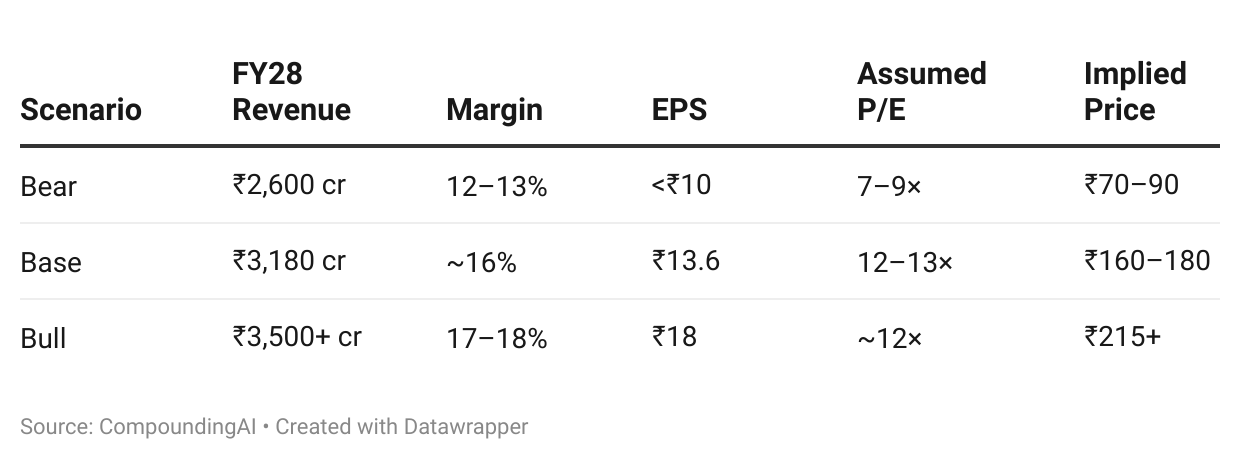

VIII. Scenario Planning: FY26–28

The credibility cycle can be mapped in three cases:

| Scenario | FY28 Revenue | Margin | EPS | Valuation Range |

|---|---|---|---|---|

| Bear | ₹2,600 cr | 12–13% | \<₹10 | Single-digit P/E |

| Base | ₹3,180 cr | \~16% | ₹13.6 | ₹160–180 |

| Bull | ₹3,500+ cr | 17–18% | ₹18 | \~₹215+ |

{kind=link}

Peer history supports this spread:

- Aarti Industries (2015–2019): base-to-bull transition through order-backed growth.

- Navin Fluorine (2020–2022): bull case rerating, then slipped into base due to execution risk.

- Atul Ltd. (2012–2022): steady base, rewarded with premium multiples for a decade.

IX. Industry Context: The Credibility Cycle

This isn’t just a company’s story. It’s about the credibility cycle in Indian chemicals:

- Promise Phase: Announce capex, talk growth.

- Bust Phase: Overpromise, underdeliver, credibility collapses.

- Repair Phase: Relearn candor, sweat capex, restore trust.

- Reward Phase: Market rerates, if execution sustains.

MOL is now in Phase 3 - Repair.

If successful, it could join the Phase 4 club with Aarti and Atul. If not, it risks languishing like peers stuck in the penalty box.

X. Epilogue: Redemption as a Compounder’s Asset

Balance sheets can recover. Margins can swing. Even plants that once ran half-empty can roar back to life. But the one asset no spreadsheet can fully capture is credibility.

For Meghmani Organics, the last two years have been a bruising reminder that growth without trust is hollow. Investors don’t just fund molecules and machinery, they fund belief. And belief, once broken, compounds in reverse.

The good news? Just like capex, credibility too can be sweated back into shape. Every quarter of honest guidance, every disclosure of risks, every incremental improvement in unit economics, these are not just numbers, but dividends of trust. Slowly, they add up. Quietly, they compound.

That’s why MOL’s story matters beyond its own ticker. It is a parable of Indian mid-cap chemicals, where promise often runs ahead of delivery, and where the rarest compounder isn’t capital, but candor.

Whether MOL ultimately joins the ranks of Aarti and Atul in the Reward Phase, or slips back into the penalty box, will depend less on chemistry than on credibility. Because in markets, as in life, trust is the compounder that never goes out of cycle.

This piece is created using inputs from CompoundingAI.

CompoundingAI is an enterprise-grade vertical intelligence engine that transforms unstructured corporate filings into decision-grade insights within minutes, complete with source-level traceability for confident, auditable workflows.

Our aim is to cut the noise & directly deliver insights.

Powered by CompoundingAI — AI research platform for Indian stocks, every claim cited from primary filings

Login Now