The GLP-1 Inflection: Why March 20 Is The "Day 1" of a New Economy

Executive Summary: The Setup

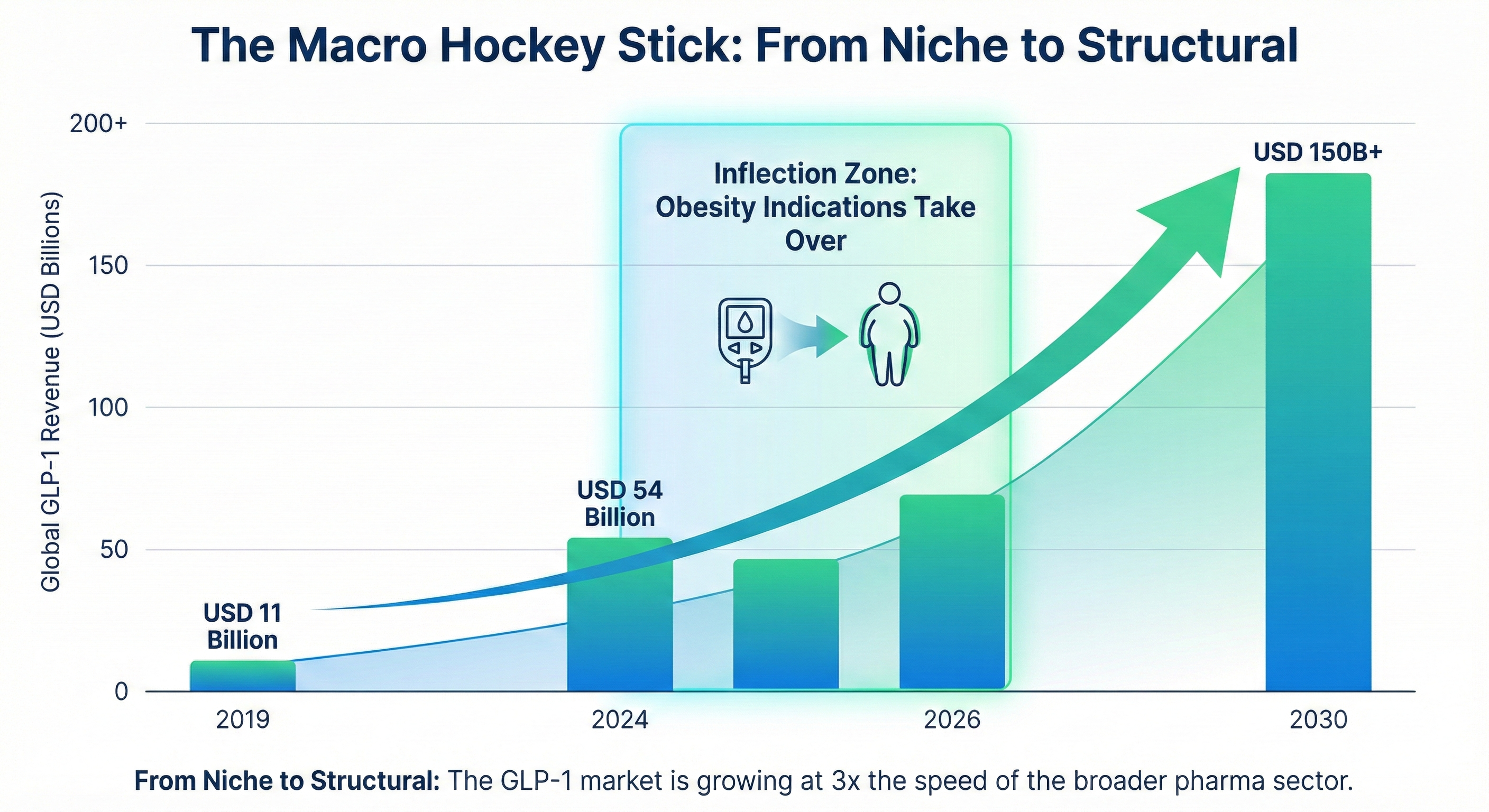

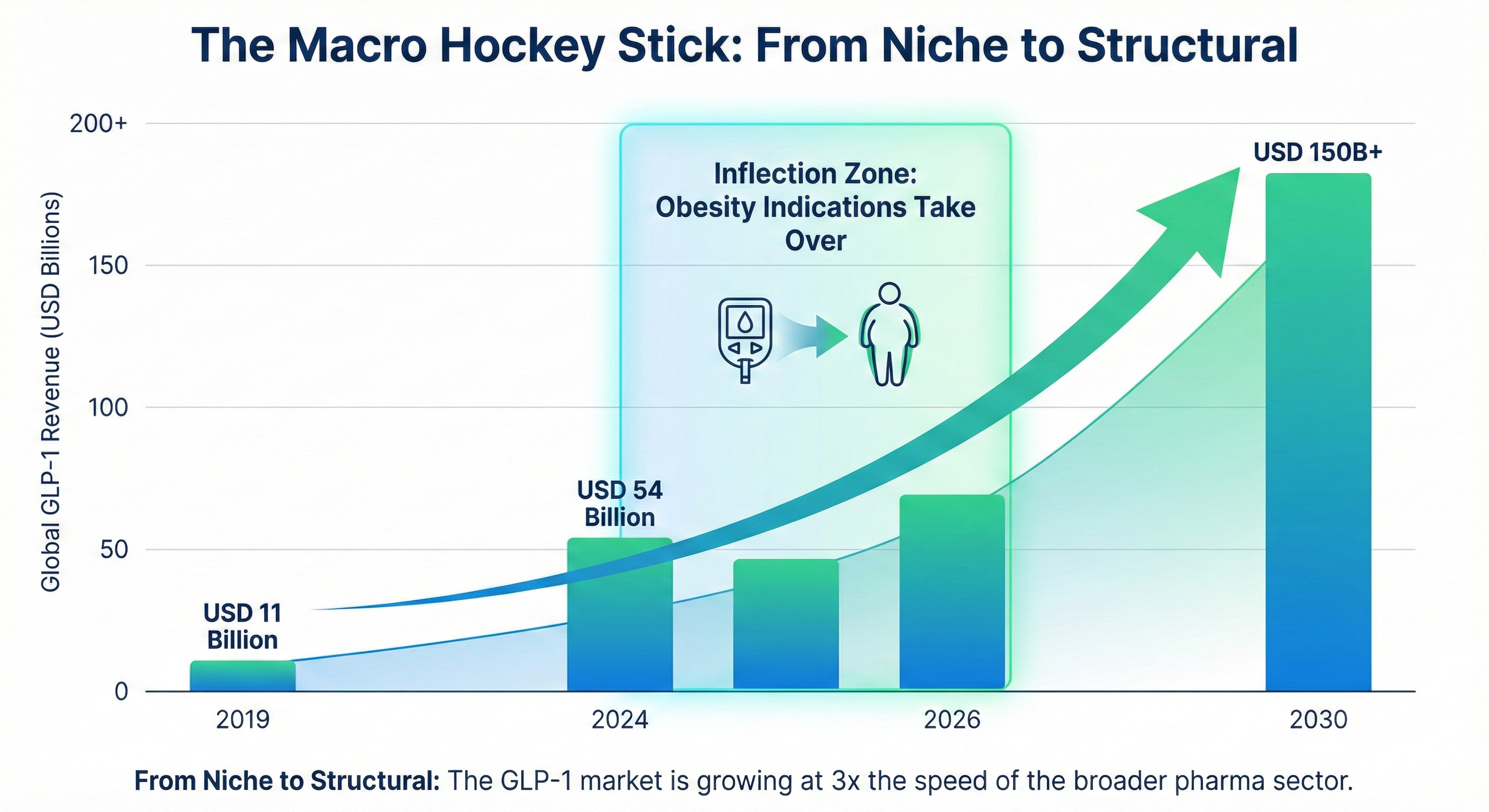

On paper, the GLP-1 market size 2026 story is a straight line up: from a USD 11 billion niche in 2019 to a potential USD 144–200 billion ecosystem by 2029. But for the sophisticated investor, the headline growth masks a violent bifurcation in obesity treatment trends.

{kind=link}

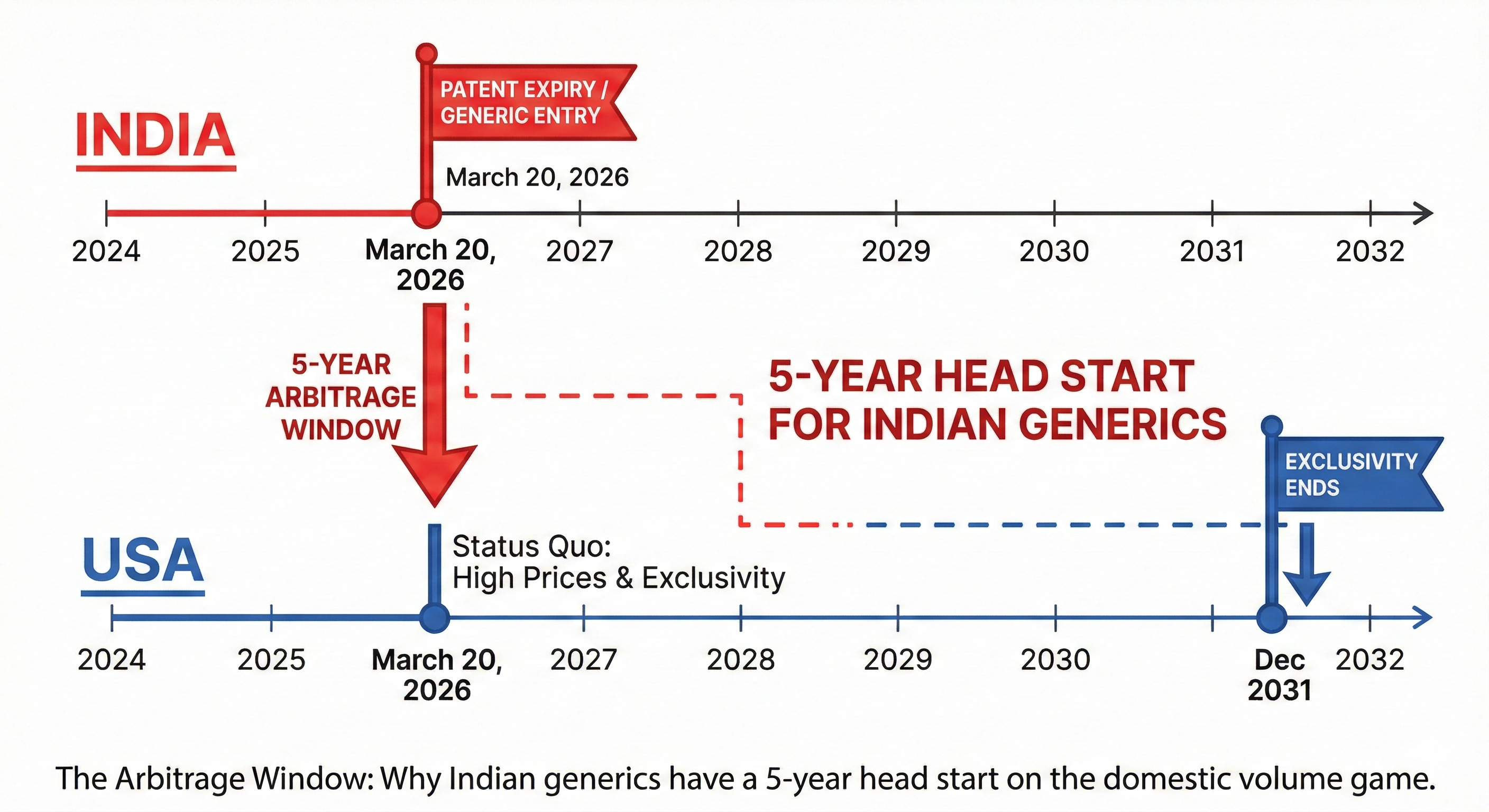

While the US market enters a period of margin compression driven by TrumpRx pricing platforms, Most-Favored-Nation (MFN) pricing risks, and Medicare coverage for GLP-1 exclusions India is barreling toward a massive “Patent Cliff” in March 2026. This date marks the expiry of the semaglutide composition patent in India (IN 262697), triggering a flood of affordable weight loss drugs and altering the profit pools for every player in the pharmaceutical supply chain.

This is a structural shift from a “scarcity” economy to a “volume” economy.

I. The Macro Thesis: The “Chronic Annuity” Model

What is GLP-1? These incretin mimetics (and dual GIP/GLP-1 co-agonists) have created a “chronic care annuity” model distinct from acute therapies. The forensic data confirms a fundamental shift:

- The Efficacy Moat: The “efficacy gap” is the primary driver of patient stickiness. Head-to-head data (tirzepatide vs semaglutide) shows weight loss efficacy reaching 20-25%, far outstripping the \~7% achieved by older generation drugs. This redefines clinical expectations beyond a simple BMI calculator to rigorous BMI staging and Adiposity-Based Chronic Disease (ABCD) management.

- The Rebound Lock-in: Real-world evidence (RWE) suggests that discontinuation leads to rapid weight regain (approx. two-thirds within a year). This transforms a patient into a lifetime subscriber, creating a recurring revenue model that supports robust Novo Nordisk revenue 2026 projections.

- From Lifestyle to Lifesaving: The label expansion into cardiovascular protection, specifically the reduction of major adverse cardiovascular events (MACE) has moved these drugs onto the insurance formulary, shifting the actuarial view from “cost” to “investment” based on proven pharmacoeconomics. Cardiovascular outcomes trials (CVOT) have cemented their role in reducing HbA1c reduction and stroke risk.

💡 Forensic Insight: The industry is effectively replacing a transactional sales model (take a pill, get cured) with a lifelong annuity model (take a shot forever). This creates “recurring revenue” quality similar to SaaS businesses, justifying higher multiples for the winners.

II. The India Catalyst: The March 2026 “Cliff”

The most significant near-term event for Indian investors is the March 2026 patent expiry. This stands in stark contrast to the US Fortress, where patent thickets may delay generic entry until 2031.

{kind=link}

The “Day 1” Scenario

- Regulatory Arbitrage: The core composition of matter patent expires in India on March 20, 2026. This creates a unique window for Indian players to democratize access domestically while the US remains locked.

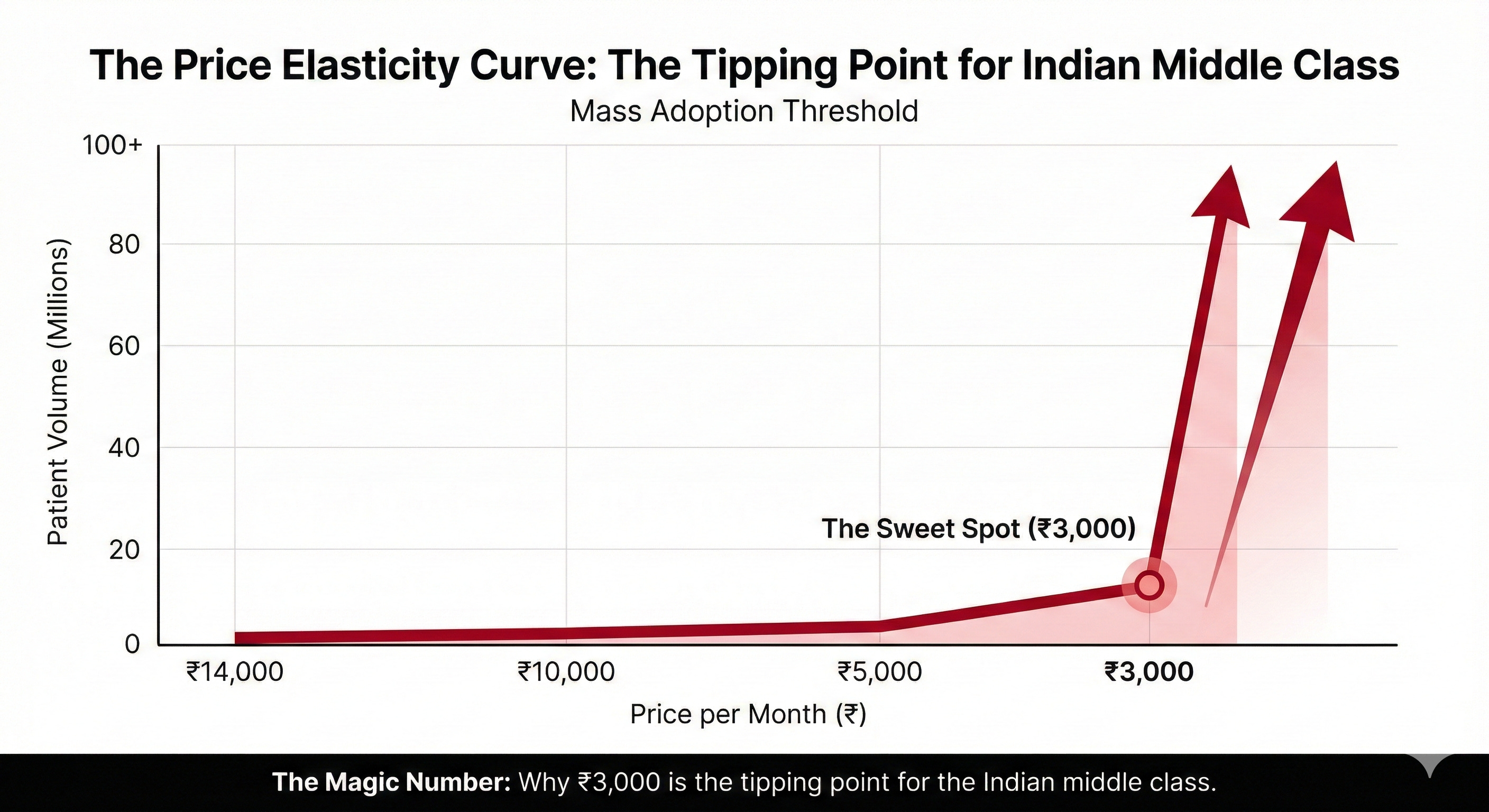

- The Price Collapse: Innovator pricing (\~₹14,000–₹26,000/month) is expected to crash to the affordable weight loss drugs threshold of ₹3,000–₹5,000/month. This GLP-1 price reduction is critical.

- Elasticity is the Key: A 70% drop in price is not just a discount; it is a market maker. It moves the addressable market from an “elite” niche (20-30 million people) to the “mass” middle class (60-100 million people).

{kind=link}

💡 The Contenders:

Sun Pharma: Planning a “Day 1” launch with brands Noveltreat and Sematrinity. Management is “very excited” and deploying a dedicated field force.

Cipla: Aiming for the “first wave,” leveraging its massive chronic therapy distribution.

Biocon: An early mover with Liraglutide already in the UK, creating a global “generic hub” strategy.

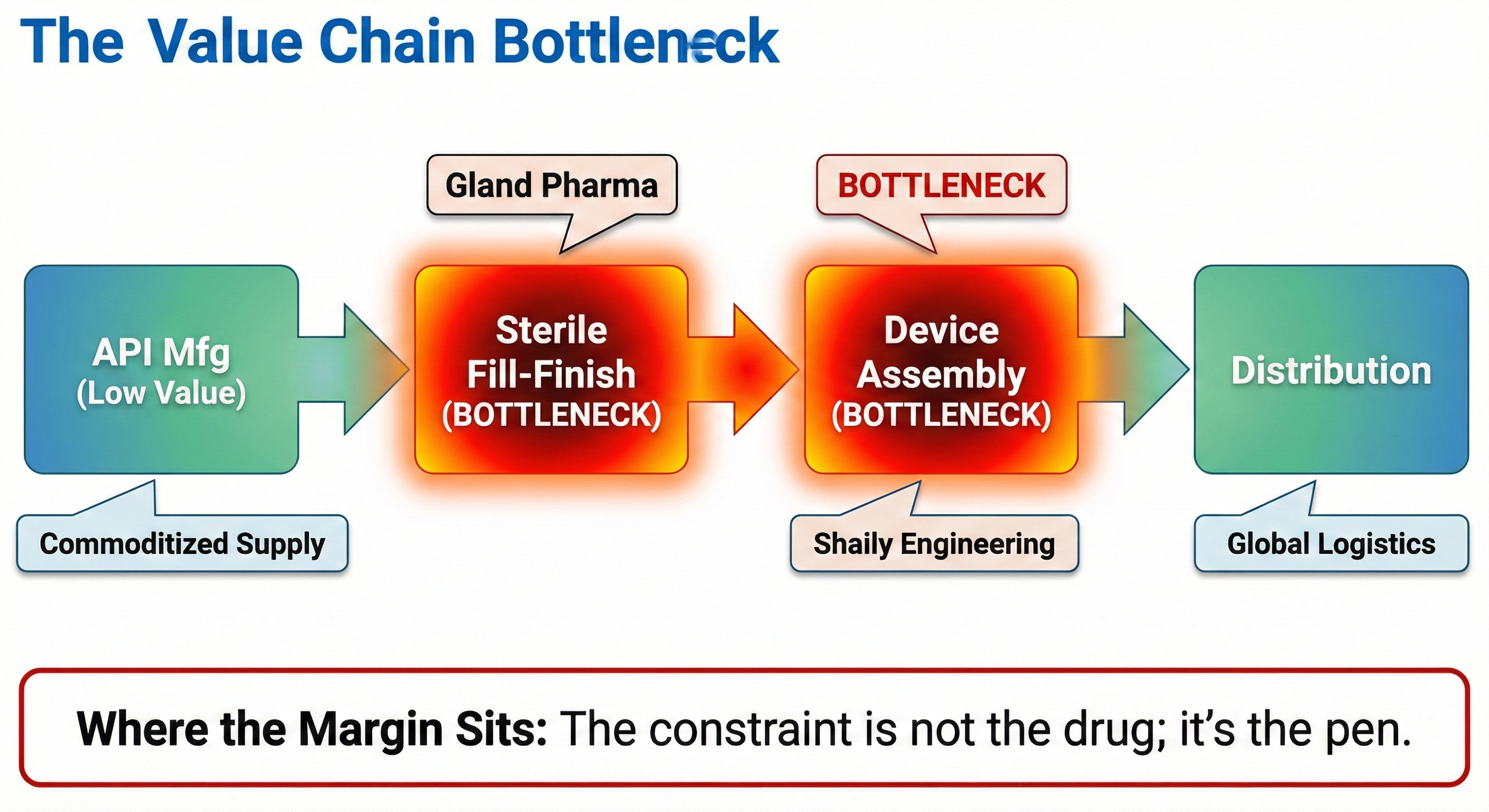

III. The “Picks and Shovels” Trade

The GLP-1 market size 2026 is not driven by acute prescription volumes alone but by the convergence of chronic disease management and complex manufacturing. This is where the investable theme emerges.

The Supply Chain Squeeze The industry is currently “short” on everything: semaglutide tablets capacity, sterile fill-finish lines, and the high-precision auto-injectors required for delivery. The barrier to entry is multi-layered.

{kind=link}

- The CDMO Opportunity: Gland Pharma is expanding pen cartridge capacity to 140 million units, making its lines “fungible” to de-risk the investment. Shaily Engineering is expanding pen capacity to 80-90 million units to solve the device bottleneck.

- Vertical Integration: Anthem Biosciences and Biocon are “fully backward integrated,” manufacturing both fermentation fragments and synthesis in-house. This is crucial for surviving the inevitable API price wars against aggressive Chinese competition.

IV. Future Outlook: Risks & Reality

The market is not static. The next wave of innovation : retatrutide clinical trials (triple agonist) and CagriSema (amylin combination) promises even higher efficacy. But the risks are structural.

Key Monitorables:

- The “TrumpRx” Effect: If the US administration enforces Most-Favored-Nation (MFN) pricing or successfully launches the TrumpRx platform for lower pricing, US margins will compress. This forces innovators like Novo Nordisk to fight harder for volume in emerging markets like India, potentially intensifying the “generic war”.

- The Oral Delay: The holy grail remains the oral tablet. However, management at OneSource Specialty Pharma projects that while oral GLP-1s will capture market share, generic oral pills are likely 8-9 years away due to robust patent protection. This secures the runway for injectable manufacturers for the next decade.

- Safety Signals: Monitoring of GLP-1 side effects (gastroparesis, muscle loss) will dictate titration schedules and patient subgroup stratification. While interest in natural GLP-1 alternatives exists, clinical data overwhelmingly favors synthetic peptides for measurable metabolic health markers.

Core Read-through

For investors, the GLP-1 story is no longer about a single molecule. It is about a metabolic health markers platform that is reshaping the pharmaceutical supply chain.

The highest return on capital over the next decade will likely sit with the owners of the “difficult” parts of the chain: the innovators with next-gen IP and the specialized manufacturers (CDMOs/Device Makers) who can solve the persistent fill-finish bottleneck. As we approach March 20, 2026, the Indian market is not just watching a patent expire; it is witnessing the birth of a mass-market metabolic economy.

Note : Not a buy/sell recommendation. For education purpose only.

This piece is created using inputs from CompoundingAI.

CompoundingAI is a vertical intelligence engine that transforms unstructured documents into decision-grade insights, complete with source-level traceability for confident, auditable workflows.

We cut the noise & directly deliver insights.

Powered by CompoundingAI — AI research platform for Indian stocks, every claim cited from primary filings

Login Now