The Rx Route: India’s Healthcare Distribution Shift and Entero’s National Ambitions

India’s Healthcare Distribution : From Fragmentation to Digital Omnipresence

India’s healthcare distribution industry, once defined by fragmented local players and logistical complexity, is now at the cusp of an evolutionary leap.

Triggered by GST-led regulatory reforms, digital transformation, and rapid consolidation, the sector is being reshaped into a more integrated, tech-enabled ecosystem.

This article provides a 360-degree analysis of the sector, spanning structural dynamics, regulatory pressures, digital adoption, margin profiles, and the growing wave of consolidation.

1. Anatomy of the Healthcare Distribution Sector: Fragmented and Complex

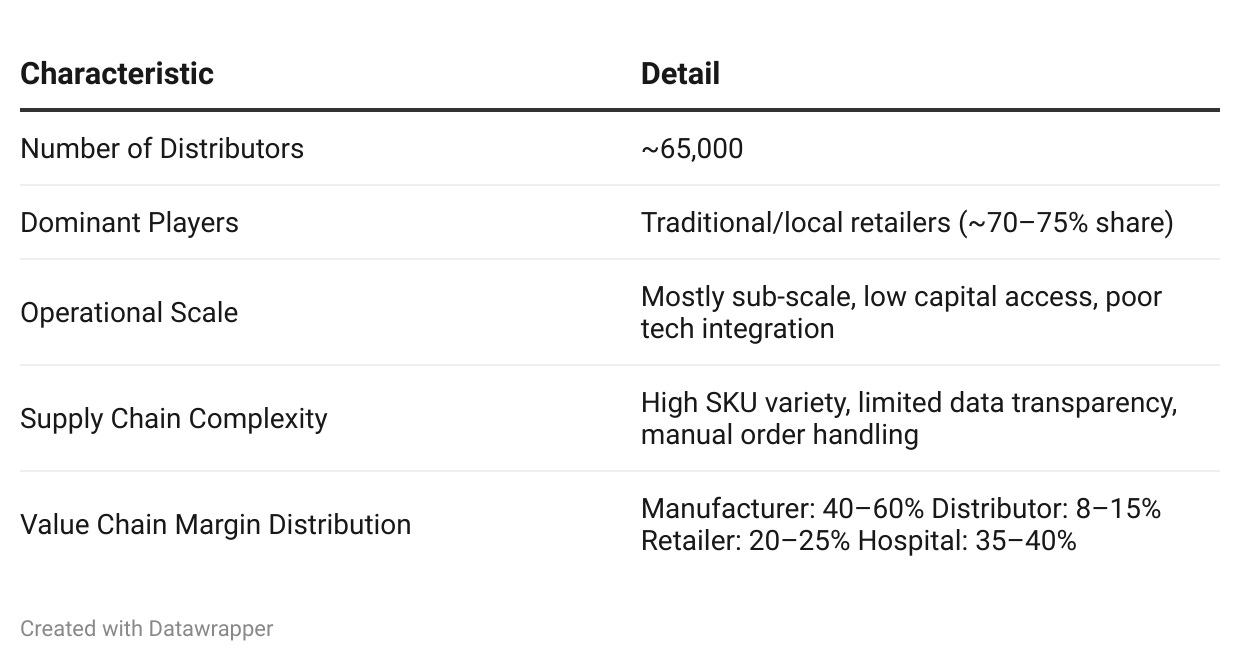

India’s healthcare distribution landscape has historically been dominated by small-scale, regionally focused distributors operating with low levels of technological adoption.

The sector's complexity is rooted in its vast geography, over 1 million pharmacies (compared to 65,000 in the US), and a fragmented supply chain where even a single molecule might have 100+ brands.

Key Structural Traits of Indian Healthcare Distribution

| Characteristic | Detail |

|---|---|

| Number of Distributors | \~65,000 |

| Dominant Players | Traditional/local retailers (\~70–75% share) |

| Operational Scale | Mostly sub-scale, low capital access, poor tech integration |

| Supply Chain Complexity | High SKU variety, limited data transparency, manual order handling |

| Value Chain Margin Distribution | Manufacturer: 40–60% Distributor: 8–15% Retailer: 20–25% Hospital: 35–40% |

{kind=link}

Operational inefficiencies plague both ends of the chain:

- Manufacturers face high product expiries and poor visibility on secondary sales.

- Retailers suffer from lower fill rates, manual order cycles, and opaque promotional schemes.

These challenges have long prevented scale and standardization, especially in northern and rural markets.

2. Regulatory Catalysts: GST and Pricing Controls Fuel Structural Change

Recent regulatory changes, especially the Goods and Services Tax (GST) and the Drug Price Control Order (DPCO), have redefined the cost structures, operational strategies, and market dynamics.

GST as a Consolidation Catalyst

- Unified taxation under GST has removed state-level distribution silos, pushing the sector toward consolidation.

- Larger players now benefit from scale, better compliance, and tech-driven efficiency.

- Companies like Entero Healthcare noted only marginal compliance costs, offset by operational benefits.

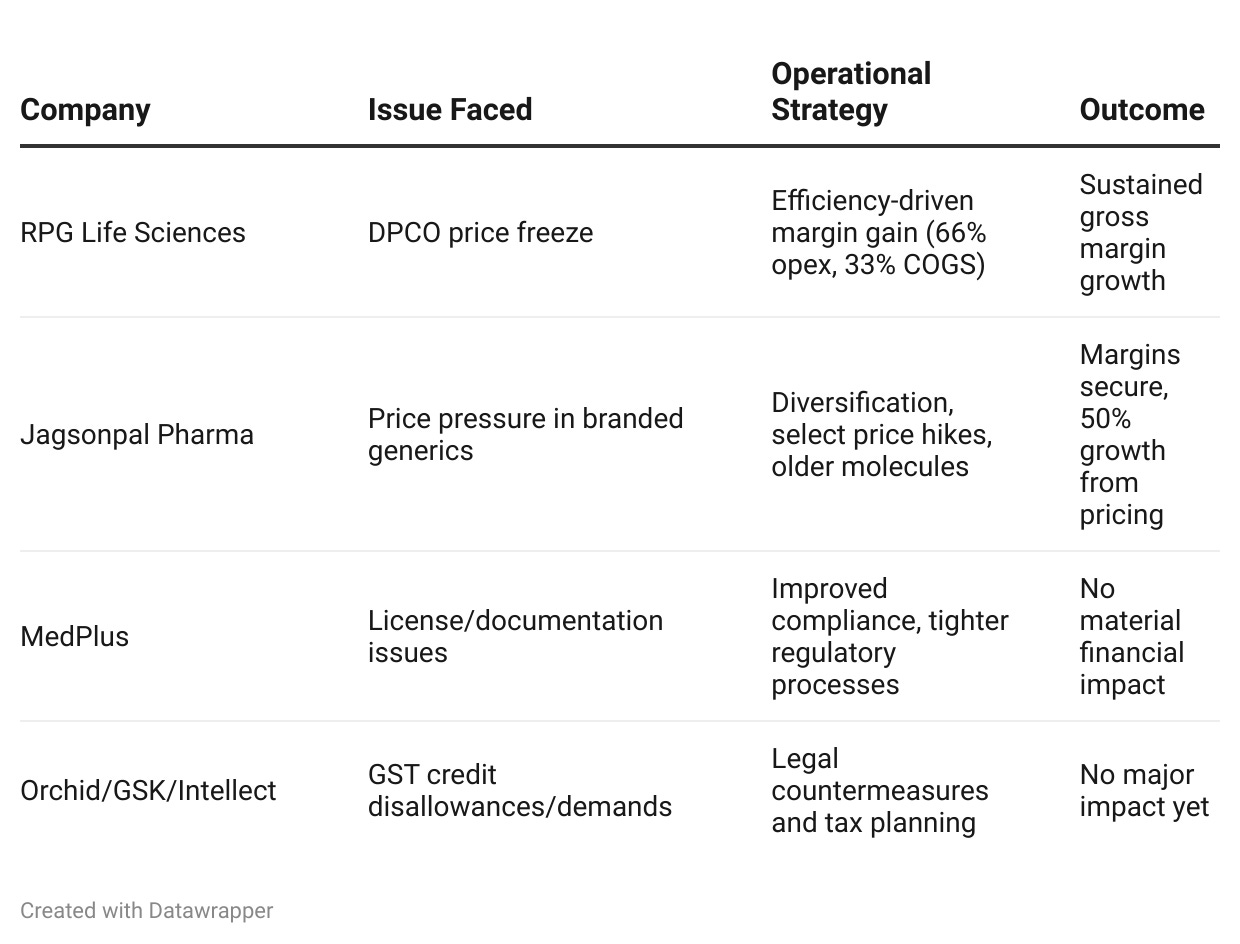

Pricing Controls and Industry Response

- RPG Life Sciences: 35% of business under DPCO, yet consistent margin improvement through opex and COGS optimization.

- Jagsonpal: Focus on older, lower-volume molecules with better price stability; price hikes contributed 50% of growth in Q1 FY26.

- MedPlus and Orchid: Encountered license and GST scrutiny but adapted via enhanced documentation and process upgrades.

Key Regulatory Challenges and Responses

| Company | Issue Faced | Operational Strategy | Outcome |

|---|---|---|---|

| RPG Life Sciences | DPCO price freeze | Efficiency-driven margin gain (66% opex, 33% COGS) | Sustained gross margin growth |

| Jagsonpal Pharma | Price pressure in branded generics | Diversification, select price hikes, older molecules | Margins secure, 50% growth from pricing |

| MedPlus | License/documentation issues | Improved compliance, tighter regulatory processes | No material financial impact |

| Orchid / GSK / Intellect | GST credit disallowances / demands | Legal countermeasures and tax planning | No major impact yet |

{kind=link}

3. Digital Disruption: Reimagining Distribution in a Tech-First World

India’s healthcare ecosystem is undergoing a digital renaissance. Telemedicine, AI-powered platforms, e-pharmacies, and supply chain digitization are becoming the new standard.

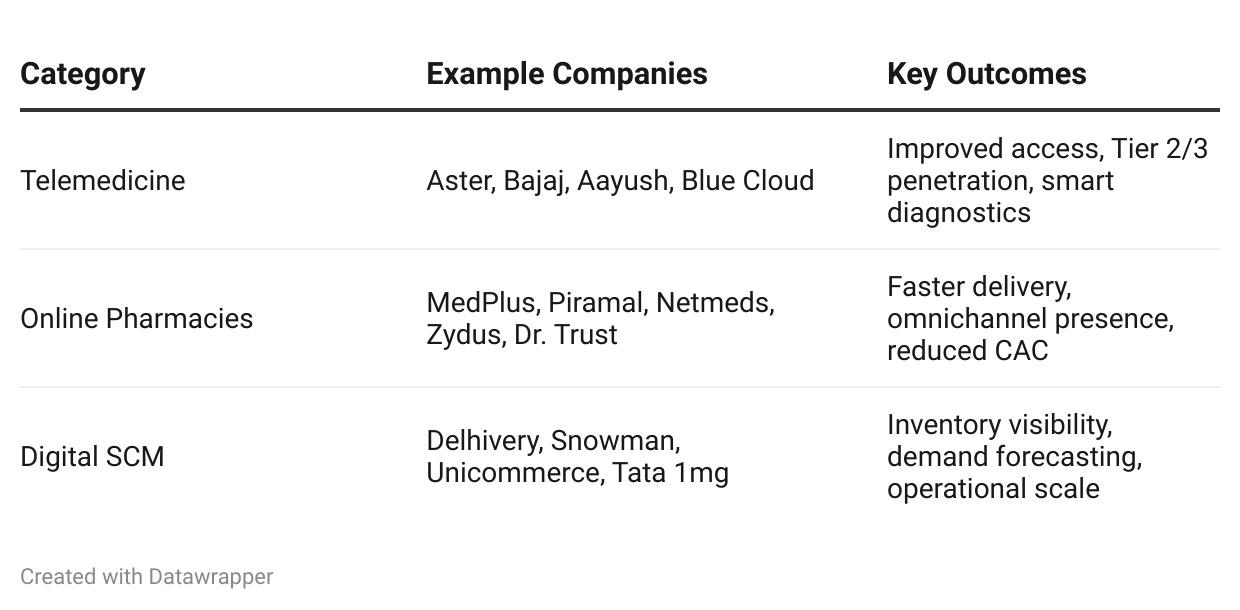

Patient Access Platforms & Telemedicine

- Aster Health App: >100,000 downloads; unifies patient care across hospitals, labs, and pharmacies.

- Bajaj Finserv Health: 5.8 million transactions in Q1 FY26 (+183% YoY); network of 130,000 doctors and 15,500 hospitals.

- Aayush Wellness: Focus on Tier 2/3 with kiosks, remote diagnostics, and healthcare ATMs; committed ₹25 crore.

- Blue Cloud: AI-led BluHealth v2.0 with facial diagnostics and remote monitoring.

Online Pharmacy Surge and Omnichannel Delivery

- MedPlus: ₹863 crore in omni-channel sales in Q1 FY26 (\~6% of revenue); 60% pickup, 40% delivery; 2,935 pincodes covered.

- Piramal Pharma: 41% YoY e-comm growth; 23% of total consumer health sales.

- Netmeds, Dr. Trust, Zydus Wellness: E-commerce and quick commerce integration to increase consumer reach.

Backend Efficiency: Digital Supply Chain and Fulfillment

- Delhivery: AI-led TMS; Express Parcel and PTL targeting 17–18% EBITDA margins.

- Snowman: Real-time cold chain visibility; tech-enhanced 5PL service delivery.

- Unicommerce + Tata 1mg: Multi-channel warehouse and order optimization across 1000+ cities.

Digital Transformation Snapshot

| Category | Example Companies | Key Outcomes |

|---|---|---|

| Telemedicine | Aster, Bajaj, Aayush, Blue Cloud | Improved access, Tier 2/3 penetration, smart diagnostics |

| Online Pharmacies | MedPlus, Piramal, Netmeds, Zydus, Dr. Trust | Faster delivery, omnichannel presence, reduced CAC |

| Digital SCM | Delhivery, Snowman, Unicommerce, Tata 1mg | Inventory visibility, demand forecasting, operational scale |

{kind=link}

4. Margin Landscape: Dissecting Profitability Across the Ecosystem

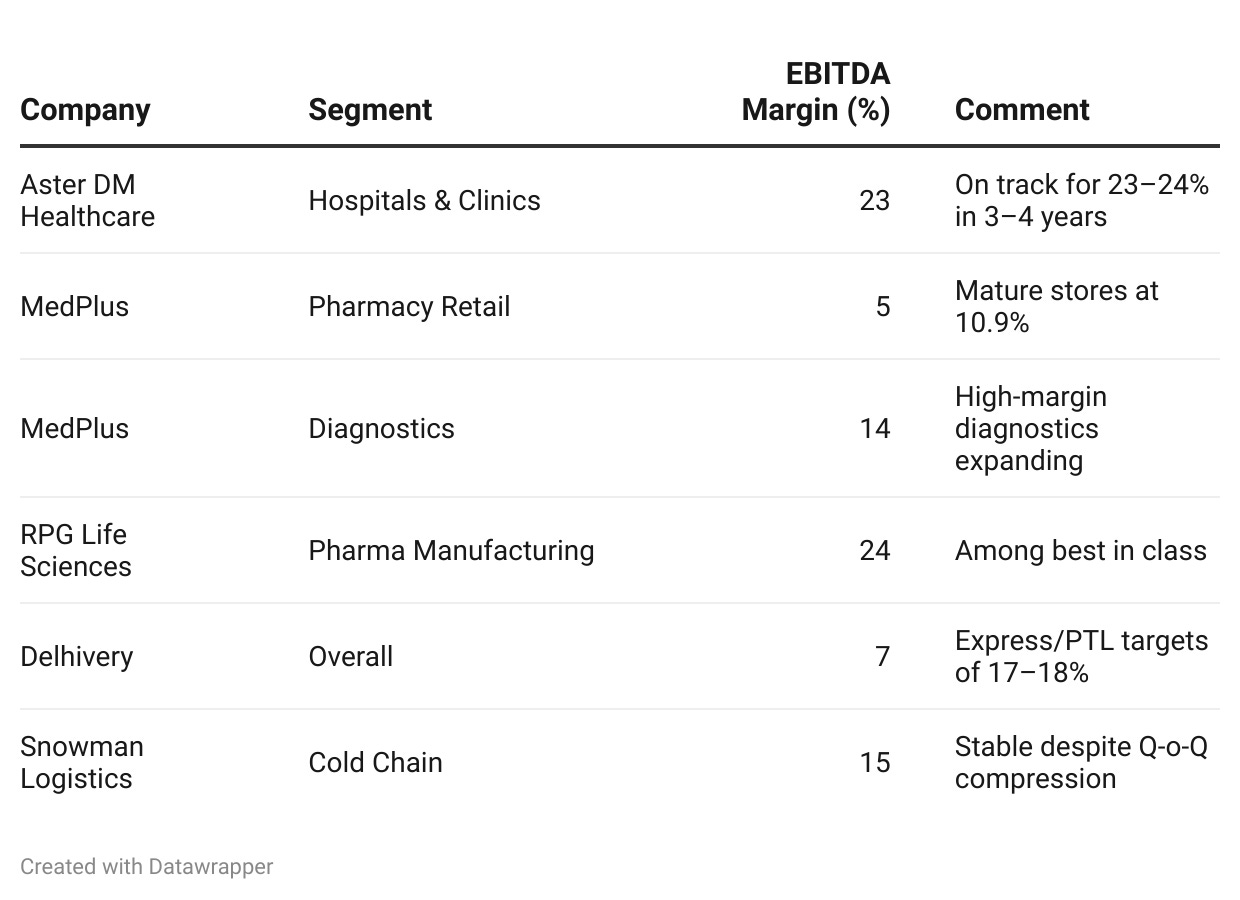

The margin architecture of the sector is shaped by business type. While pharmacy retail margins remain modest, diagnostics, hospitals, logistics, and pharma manufacturing enjoy higher EBITDA spreads.

Operating Margins (EBITDA)

| Company | Segment | EBITDA Margin (%) | Comment |

|---|---|---|---|

| Aster DM Healthcare | Hospitals & Clinics | 23 | On track for 23–24% in 3–4 years |

| MedPlus | Pharmacy Retail | 5 | Mature stores at 10.9% |

| MedPlus | Diagnostics | 14 | High-margin diagnostics expanding |

| RPG Life Sciences | Pharma Manufacturing | 24 | Among best in class |

| Delhivery | Overall | 7 | Express/PTL targets of 17–18% |

| Snowman Logistics | Cold Chain | 15 | Stable despite Q-o-Q compression |

{kind=link}

Operational leverage, portfolio rebalancing, and digital integration are pushing margins upward, especially in high-value segments.

5. Consolidation: M\&A Wave Reshaping the Industry

The era of solo operators is fading fast. India’s healthcare distribution is consolidating rapidly into fewer, more scalable, omnichannel players.

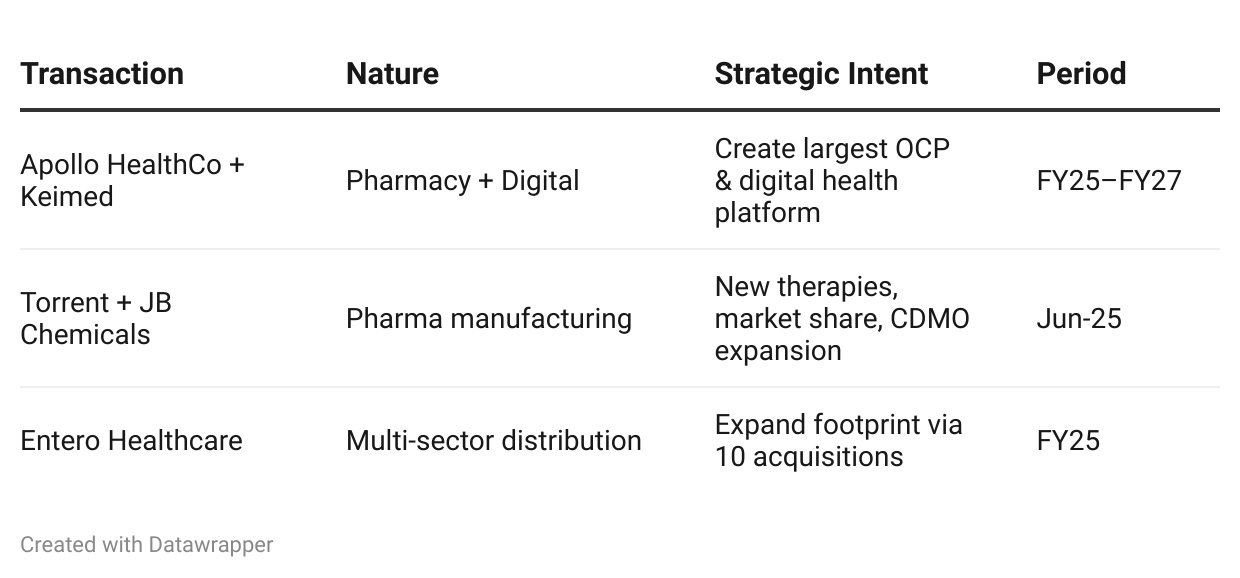

Key Transactions

- Apollo HealthCo + Keimed: Combined revenue of ₹16,267 crore in FY25, targeting ₹25,000 crore by FY27.

- Torrent Pharma + JB Chemicals: Entry into ophthalmology, CDMO, and stronger India market footprint.

- Entero Healthcare: Completed 10 strategic acquisitions in FY25, contributing ₹792 crore in annualized revenue, enhancing footprint across diagnostics, medical devices, and pharma segments.

Drivers of Consolidation

- GST regime and pan-India tax standardization

- Operational synergies and therapy diversification

- Investor appetite for scaled models and vertical integration

- Fragmentation in diagnostics and offline retail inviting M\&A interest

Consolidation Highlights

| Transaction | Nature | Strategic Intent | Period |

|---|---|---|---|

| Apollo HealthCo + Keimed | Pharmacy + Digital | Create largest OCP & digital health platform | FY25–FY27 |

| Torrent + JB Chemicals | Pharma manufacturing | New therapies, market share, CDMO expansion | Jun-25 |

| Entero Healthcare | Multi-sector distribution | Expand footprint via 10 acquisitions | FY25 |

{kind=link}

Scaling with Governance: Inside Entero Healthcare’s Execution Engine

Entero Healthcare Solutions Ltd. (Entero) is transforming India’s fragmented healthcare distribution landscape into a tech-integrated, scalable, and acquisition-led platform.

With a proven track record of rapid expansion, operational discipline, and margin-accretive acquisitions, Entero is shaping up to become a national leader in pharmaceutical, medical device, and consumables distribution.

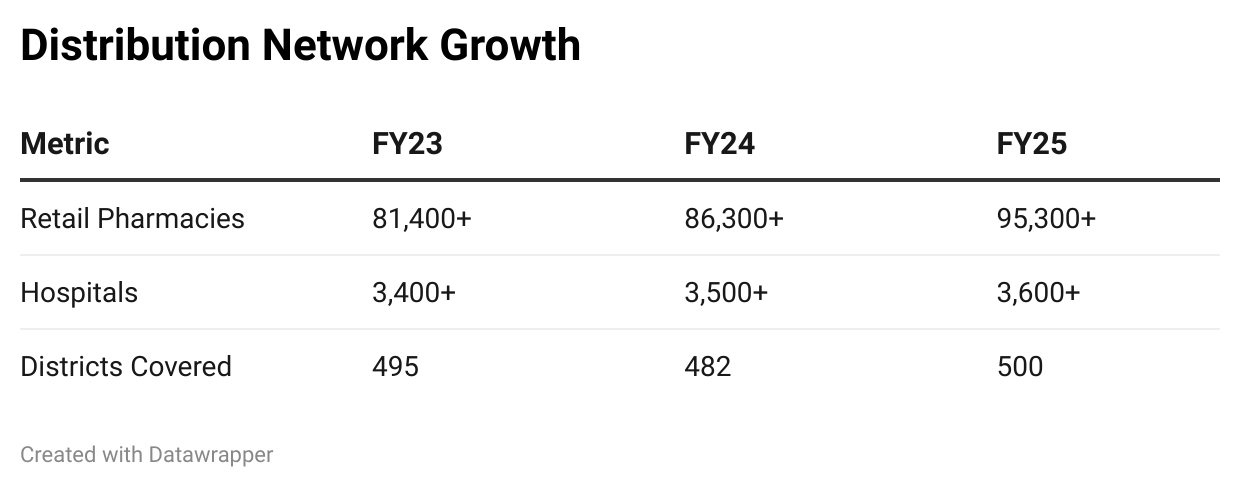

1. Geographic Expansion and Distribution Footprint

In an industry where distribution efficiency dictates reach, Entero has established itself as a dominant national player. Operating across 20 states, 44 cities, and 500 districts, its client base includes over 95,300 retail pharmacies and 3,600 hospitals as of FY25.

| Metric | FY23 | FY24 | FY25 |

|---|---|---|---|

| Retail Pharmacies | 81,400+ | 86,300+ | 95,300+ |

| Hospitals | 3,400+ | 3,500+ | 3,600+ |

| Districts Covered | 495 | 482 | 500 |

{kind=link}

The consistent increase in retail pharmacy and hospital coverage reflects Entero’s granular expansion strategy. The minor dip in FY24 districts highlights consolidation efforts, followed by a robust expansion in FY25.

The roadmap to 150,000–200,000 retail customers further emphasizes Entero’s ambition to lead in both depth and breadth of reach.

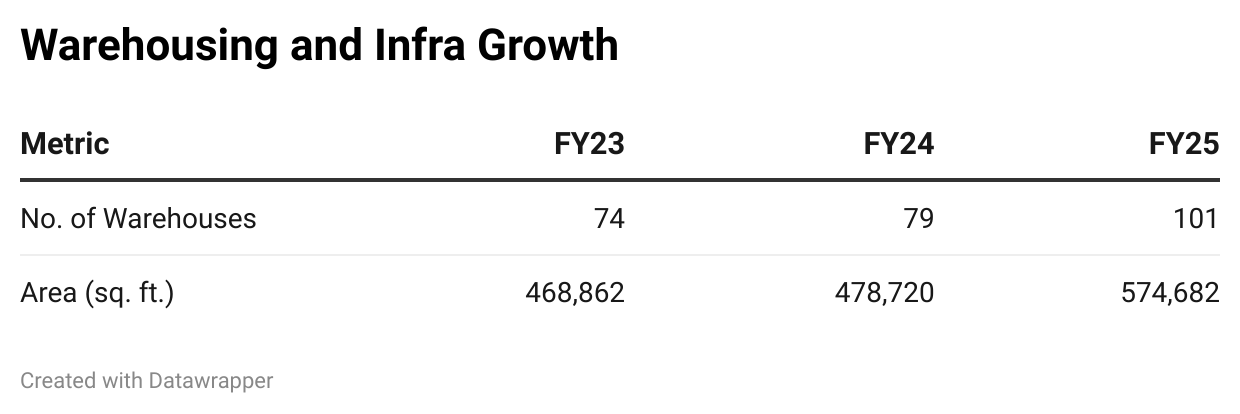

2. Warehousing and Infrastructure Growth

Entero’s logistics backbone is reinforced by its rapidly expanding warehousing network, critical for nationwide fulfilment.

| Metric | FY23 | FY24 | FY25 |

|---|---|---|---|

| No. of Warehouses | 74 | 79 | 101 |

| Area (sq. ft.) | 4,68,862 | 4,78,720 | 5,74,682 |

{kind=link}

The 27-warehouse expansion in two years aligns with growing SKU complexity and geographic reach. This physical scale ensures lower delivery times, better inventory coverage, and supports compliance with Good Distribution Practices (GDP).

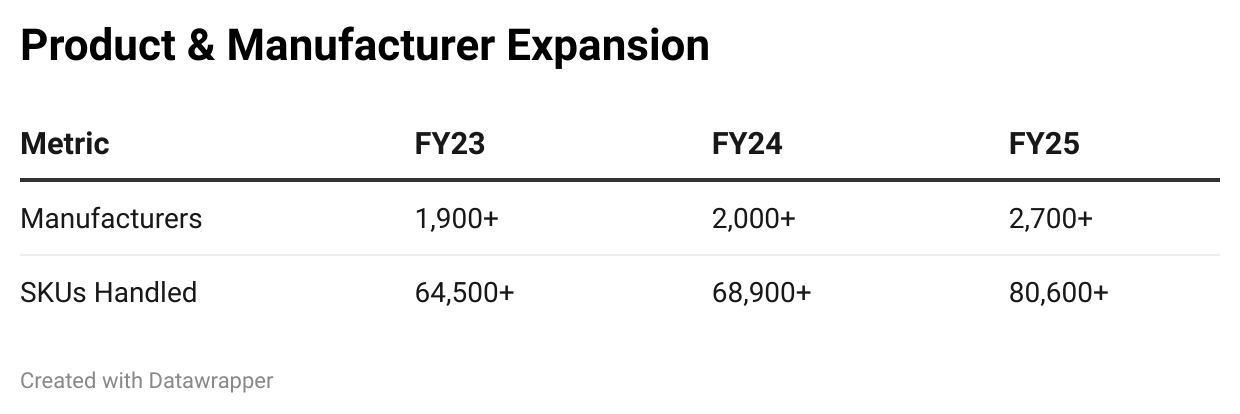

3. Manufacturer Relationships and SKU Depth

Entero’s growing portfolio of SKUs and manufacturer relationships signals its ability to cater to India’s diverse healthcare demands.

| Metric | FY23 | FY24 | FY25 |

|---|---|---|---|

| Manufacturers | 1,900+ | 2,000+ | 2,700+ |

| SKUs Handled | 64,500+ | 68,900+ | 80,600+ |

{kind=link}

A 42% increase in SKU count and 800+ new manufacturers in two years indicates strong onboarding capabilities and high trust among suppliers.

This diversity also insulates the company from supply shocks and empowers regional customizations.

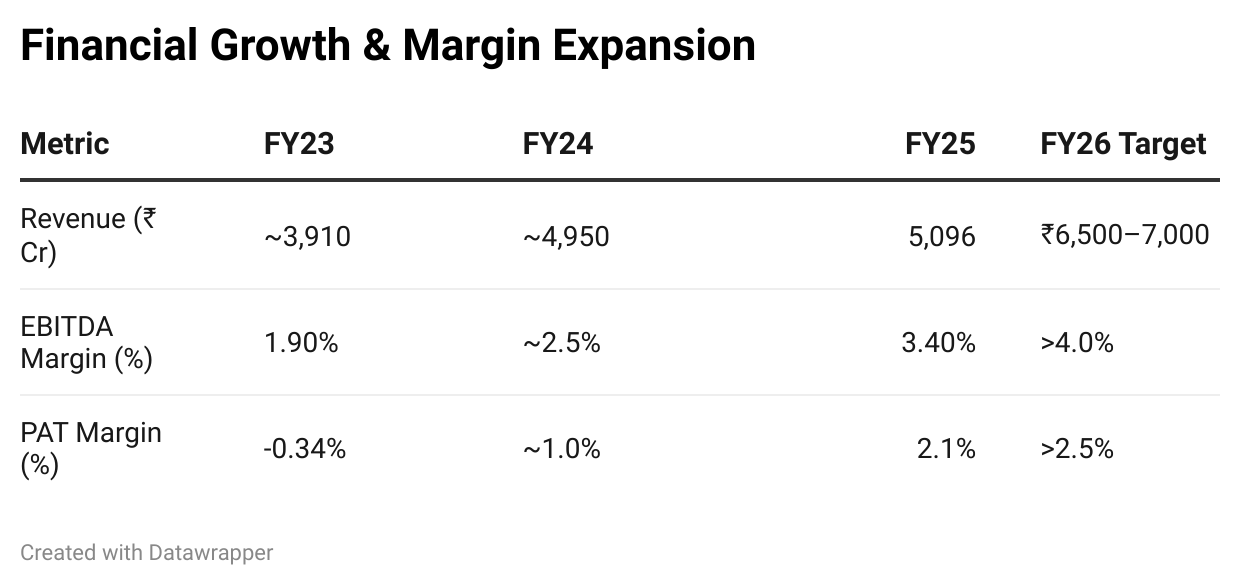

4. Financial Growth & Profitability Trends

Entero has transitioned from scale-first growth to margin-focused consolidation, as seen in its profitability trajectory.

| Metric | FY23 | FY24 | FY25 | FY26 Target |

|---|---|---|---|---|

| Revenue (₹ Cr) | \~3,910 | \~4,950 | 5,095.80 | ₹6,500–7,000 |

| EBITDA Margin (%) | 1.90% | \~2.5% | 3.40% | >4.0% |

| PAT Margin (%) | -0.34% | \~1.0% | 2.10% | >2.5% |

{kind=link}

Margin expansion has outpaced revenue growth, enabled by scale benefits, centralized procurement, and technology-led integration of acquisitions.

The PAT turnaround reflects stronger cost controls and strategic debt reduction.

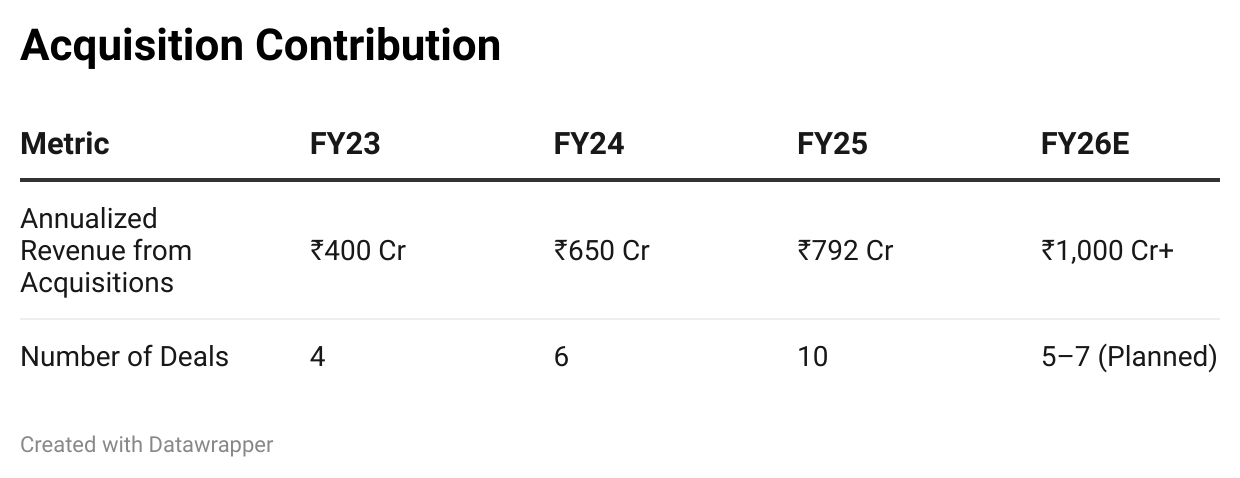

5. Acquisition Strategy: Scale via Consolidation

Entero’s core differentiation lies in its disciplined and strategic M\&A program.

| Metric | FY23 | FY24 | FY25 | FY26E |

|---|---|---|---|---|

| Annualized Revenue from Acquisitions | ₹400 Cr | ₹650 Cr | ₹792 Cr | ₹1,000 Cr+ |

| Number of Deals | 4 | 6 | 10 | 5–7 (Planned) |

{kind=link}

With over 50 bolt-on acquisitions since inception, Entero has refined a playbook of acquiring sub-scale distributors at reasonable EV/EBITDA multiples, preserving regional goodwill, and integrating through its tech backbone.

FY26's target implies inorganic growth could contribute 15–18% to top-line.

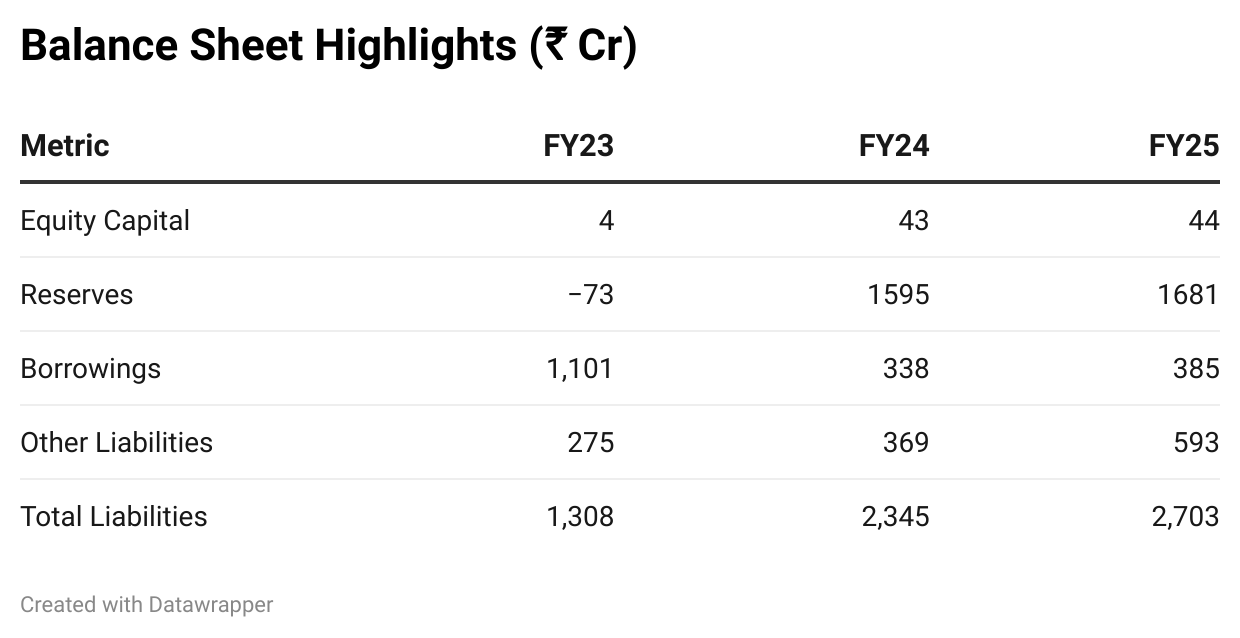

6. Leverage, Working Capital & Cash Flow Management

Despite its acquisition-heavy model, Entero has exercised balance sheet prudence.

| Metric | FY23 | FY24 | FY25 |

|---|---|---|---|

| Equity Capital | 4 | 43 | 44 |

| Reserves | -73 | 1,595 | 1,681 |

| Borrowings | 1,101 | 338 | 385 |

| Other Liabilities | 275 | 369 | 593 |

| Total Liabilities | 1,308 | 2,345 | 2,703 |

{kind=link}

The IPO-funded equity base and profits have significantly boosted net worth. Moderate debt increase in FY25 supports M\&A and CapEx without straining leverage.

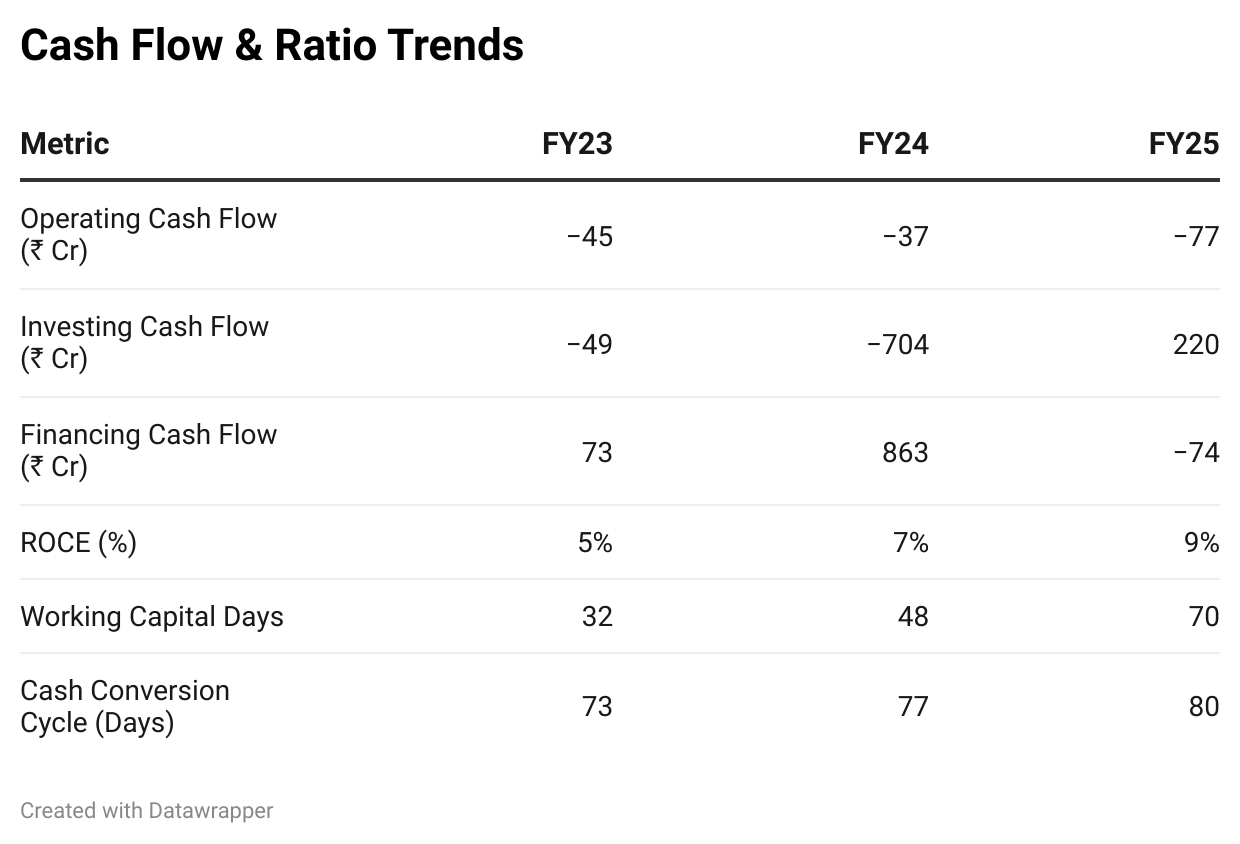

| Metric | FY23 | FY24 | FY25 |

|---|---|---|---|

| Operating Cash Flow (₹ Cr) | -45 | -37 | -77 |

| Investing Cash Flow (₹ Cr) | -49 | -704 | 220 |

| Financing Cash Flow (₹ Cr) | 73 | 863 | -74 |

| ROCE (%) | \~2.3% | \~4.7% | \~9.2% |

| Working Capital Days | 32 | 48 | 70 |

| Cash Conversion Cycle (Days) | 73 | 77 | 80 |

{kind=link}

CapEx-related outflows peaked in FY24; FY25 saw improved investment cash flow.

ROCE has improved significantly from 1% in FY22 to 9% in FY25, marking a 9x improvement.

Even on a more recent basis, ROCE rose from 5% in FY23 to 9% in FY25, driven by better operating margins, post-acquisition integration synergies, and disciplined capital management.

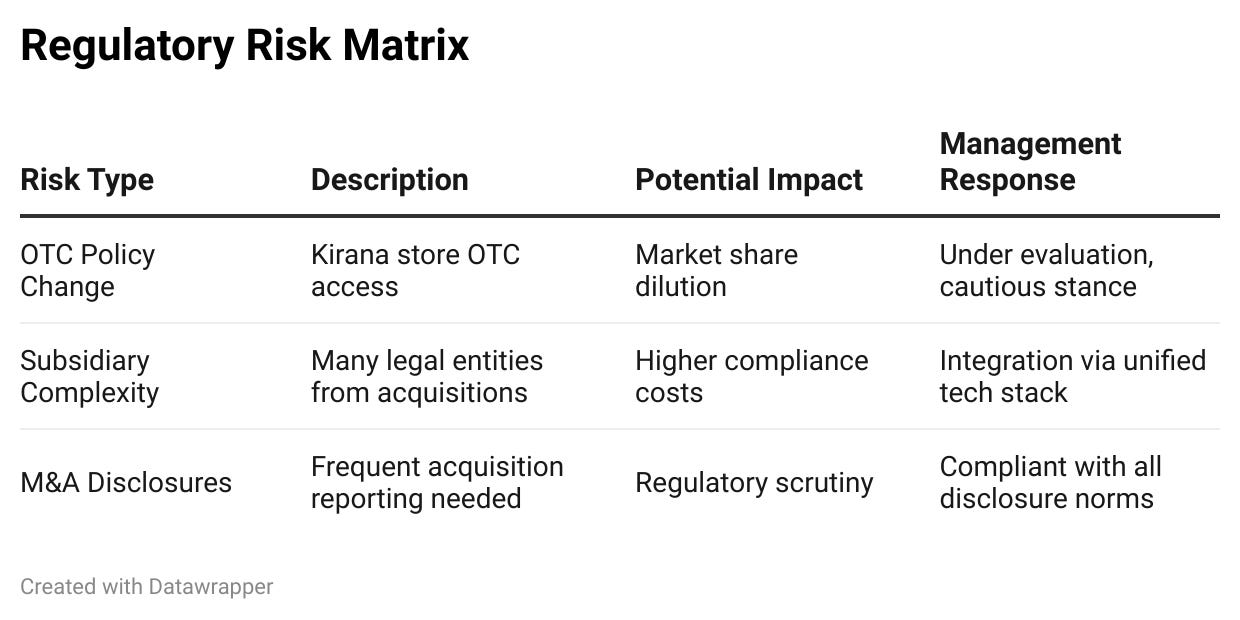

7. Regulatory and Compliance Risk Management

Entero operates in a tightly regulated industry and has responded with proactive compliance and adaptability.

| Risk Type | Description | Potential Impact | Management Response |

|---|---|---|---|

| OTC Policy Change | Kirana store OTC access | Market share dilution | Under evaluation, cautious stance |

| Subsidiary Complexity | Many legal entities from acquisitions | Higher compliance costs | Integration via unified tech stack |

| M\&A Disclosures | Frequent acquisition reporting needed | Regulatory scrutiny | Compliant with all disclosure norms |

{kind=link}

Entero remains cautious around the potential OTC policy liberalization.

While its multi-subsidiary model increases compliance cost, the company continues to retain local branding advantages, with back-end processes unified.

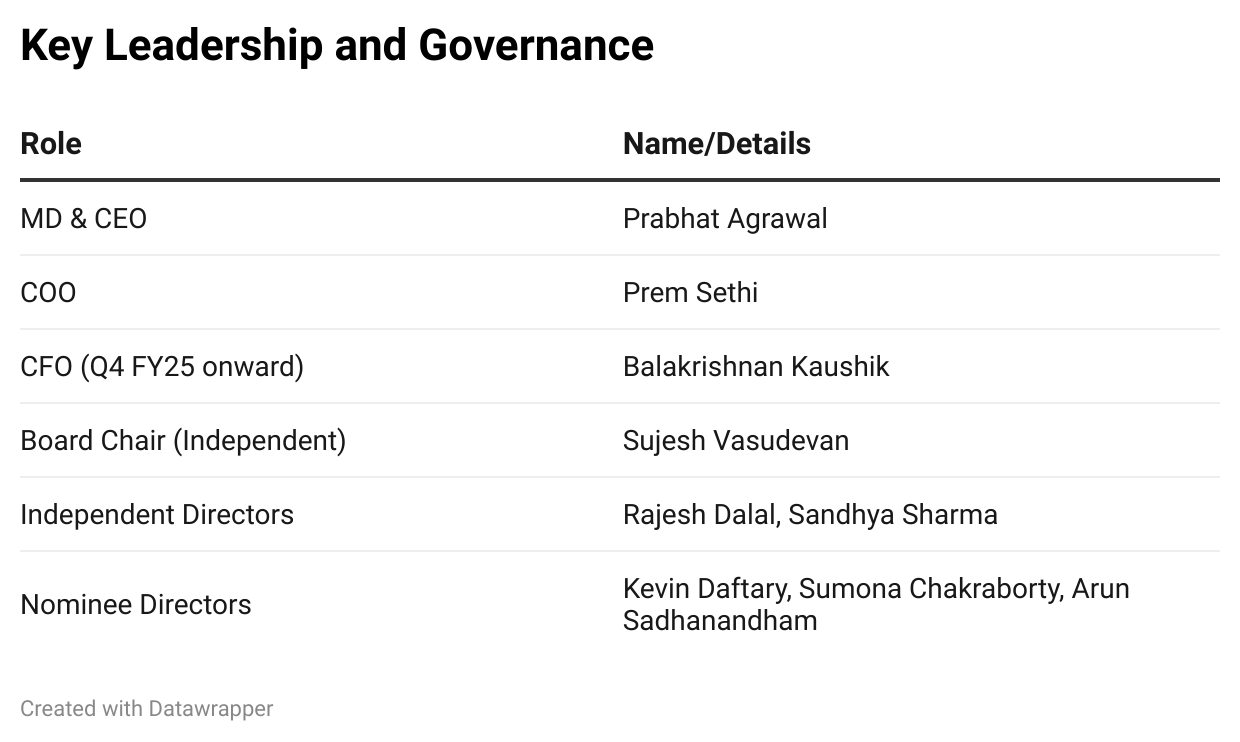

8. Corporate Governance and Leadership Stability

Strong institutional backing and operational leadership have been the cornerstones of Entero’s governance structure.

| Role | Name/Details |

|---|---|

| MD & CEO | Prabhat Agrawal |

| COO | Prem Sethi |

| CFO (Q4 FY25 onward) | Balakrishnan Kaushik |

| Board Chair (Independent) | Sujesh Vasudevan |

| Independent Directors | Rajesh Dalal, Sandhya Sharma |

| Nominee Directors | Kevin Daftary, Sumona Chakraborty, Arun Sadhanandham |

{kind=link}

Recent Changes:

- CFO transitioned from C.V. Ram to Kaushik in FY25.

- Director Vipul Desai exited in May 2024.

The presence of multiple independent directors supports robust governance and oversight, while nominee directors reflect investor alignment.

While Entero’s board composition appears structurally sound, investors should continue monitoring succession planning and audit committee independence as M\&A activity scales.

9. Scalability Outlook: A Platform for Healthcare Consolidation

Entero is rapidly formalizing India’s fragmented and inefficient healthcare distribution network by:

- Operating a tech-first B2B platform (Entero Direct).

- Scaling via targeted bolt-on acquisitions.

- Maintaining strong unit economics and margin expansion.

- Building warehousing and SKU infrastructure that’s future-ready.

- Proactively adapting to regulatory and industry shifts.

Entero Healthcare Solutions Ltd. is building a national distribution infrastructure that could reshape Indian healthcare logistics.

While the company has shown strong execution across growth, integration, and governance, investor vigilance is warranted around working capital discipline and the complexity of its M\&A-driven model.

Note : No Buy/Sell recommendation. Purely for educational purposes.

This piece is created using CompoundingAI’s chat & forensic reports

CompoundingAI is an enterprise-grade vertical intelligence engine that transforms unstructured corporate filings into decision-grade insights within minutes, complete with source-level traceability for confident, auditable workflows.

Powered by CompoundingAI — AI research platform for Indian stocks, every claim cited from primary filings

Login Now