Why do rich people invest millions in art ? Some thoughts.

Last week, a 130-year-old painting sold at a Mumbai auction for ₹167.2 crore.

The estimate was ₹80 crore. It went for double.

Everyone reported the number. Nobody asked the obvious question - not because it’s a secret, but because in certain circles, it’s considered impolite.

The Peculiar Economics of Art

There’s a reason serious money has always found its way into paintings, sculptures, and antiquities and it has less to do with aesthetics than people admit.

Most assets have a reference price. You can look up what a flat in Bandra sold for last month. You can pull up the last traded price of an HDFC Bank share. Auditors, tax authorities, and regulators can do the same.

A painting has no reference price except the last time someone sold one. And that last sale was whatever two people in a room decided it was worth. No formula, no comparable transaction database, no DCF model that holds up in court.

This makes art genuinely different from almost everything else a wealthy family can own.

When a painting sells at public auction, that price becomes legally real - a documented, taxable market event. The proceeds are clean from the moment the hammer falls. The buyer paid, the seller received, tax gets computed on the gain. Everything is above board.

The question nobody asks is what happened before the auction.

How the Gap Gets Explained Away

The ₹87 crore above the upper estimate gets described as “passion,” “competition,” “the market maturing.” All plausible. Indian wealth has genuinely grown. Cultural pride in domestic art is real. Diaspora collectors are active. These are not invented explanations.

But there’s a parallel explanation that’s equally consistent with the data, and it comes from the regulatory world rather than the art world.

The FATF - the body that sets global anti-money laundering standards has for years flagged high-value art as the major asset class with the weakest oversight. Auction houses in India are not designated reporting entities under PMLA the way banks, brokers, and even real estate registration authorities are. This means no mandatory KYC on bidders, no beneficial ownership disclosure, and no suspicious transaction reporting requirements for art transactions.

Which means: if you needed to move capital from one form to another - say, from privately held cash to publicly documented wealth and you wanted to do it at scale, art is the most efficient instrument available. You pay tax on the gain. Everything is reported. The money is clean on the other side.

The “overpay” above fair value isn’t irrational in this context. It’s the cost of the service.

Some Documented Context

This isn’t a new observation or an Indian-specific one. The cases that have actually been prosecuted globally give a sense of the pattern.

A Brazilian financier in the early 2000s moved embezzled funds through a collection of high-value works, including a Basquiat he tried to bring into the US with paperwork declaring its value at $100. The painting was eventually seized, but extracting it took over a decade of legal proceedings across two countries.

The 1MDB fraud in Malaysia, which ran into the billions, involved acquiring a $35 million Picasso and a $107 million Basquiat through private sales and shell companies. Art was a deliberate choice - portable, subjectively priced, and hard to trace.

Mexico introduced buyer identification requirements for art purchases in the early 2010s. The market dropped 70% the following year. Cultural enthusiasm, apparently, was more elastic than expected.

The EU responded to all of this in 2020 by bringing auction houses under the same AML framework as financial institutions - mandatory KYC, ownership disclosure, transaction monitoring. India has not moved in this direction.

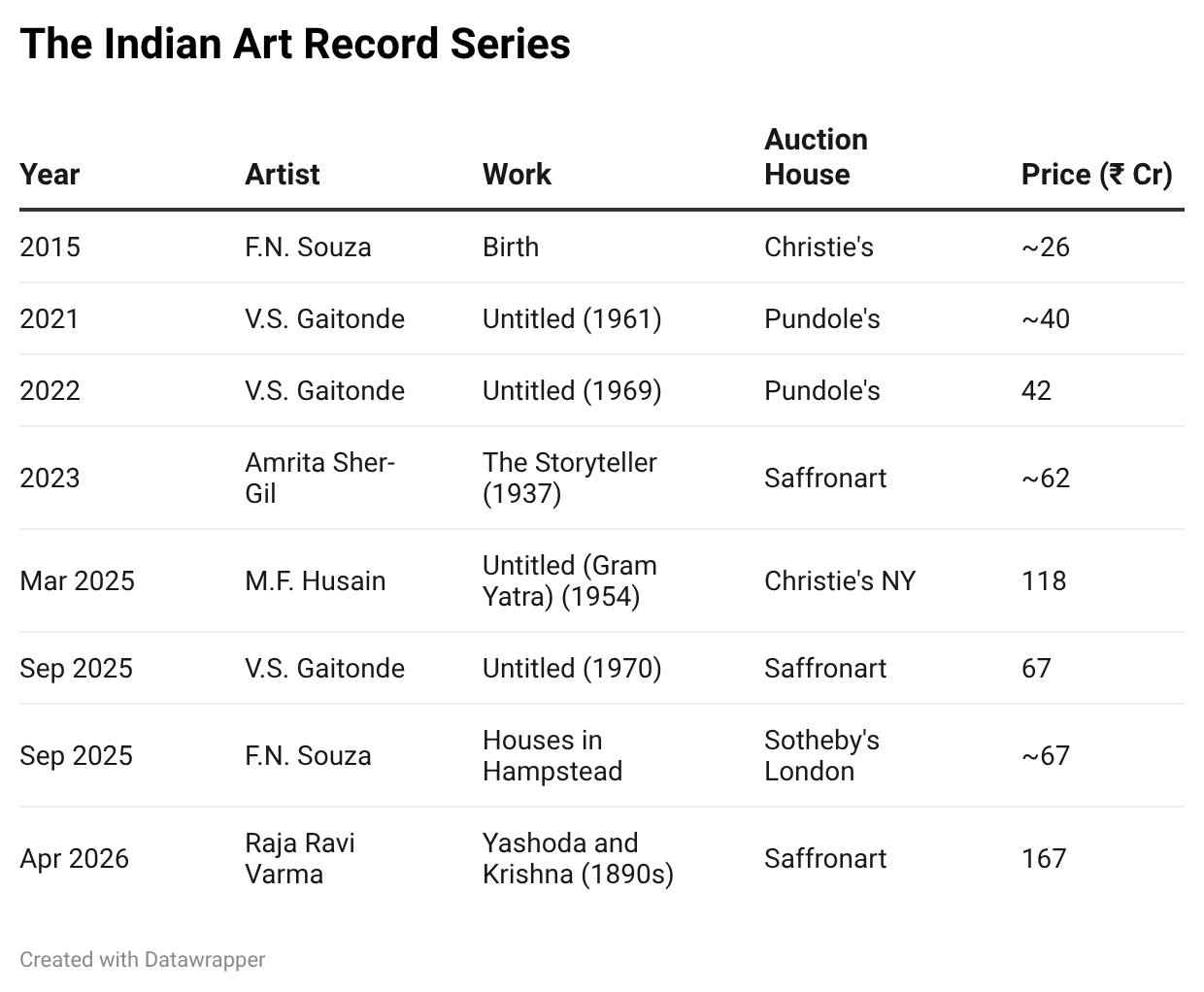

The Indian Record Series

| Year | Artist | Work | Auction House | Price (₹ Cr) |

|---|---|---|---|---|

| 2015 | F.N. Souza | Birth | Christie's | \~26 |

| 2021 | V.S. Gaitonde | Untitled (1961) | Pundole's | \~40 |

| 2022 | V.S. Gaitonde | Untitled (1969) | Pundole's | 42 |

| 2023 | Amrita Sher-Gil | The Storyteller (1937) | Saffronart | \~62 |

| Mar 2025 | M.F. Husain | Untitled (Gram Yatra) (1954) | Christie's NY | 118 |

| Sep 2025 | V.S. Gaitonde | Untitled (1970) | Saffronart | 67 |

| Sep 2025 | F.N. Souza | Houses in Hampstead | Sotheby's London | \~67 |

| Apr 2026 | Raja Ravi Varma | Yashoda and Krishna (1890s) | Saffronart | 167 |

For context, here’s what the top end of the Indian art market has done over the past decade - all figures from verified public auction records:

{kind=link}

The Husain in March 2025 sold for four times its high estimate. Christie’s own head of South Asian art publicly advised the market not to extrapolate from that result. The Gaitonde in September sold for three times its estimate. The Ravi Varma last week - double.

It’s worth noting that insiders at these auctions have observed the same small set of buyers driving most of the top-end action. One London dealer, covering Art Mumbai in late 2025, noted that “many exhibitors in the modern section were waiting on the same few key figures to show up.” A thin buyer pool consistently pushing prices well above estimates is not how a normal market behaves.

It might just mean Indian collectors are very enthusiastic. It might mean something else.

What Happens After : The Financial Structure

A public auction record doesn’t just set a price. It creates a reference rate for everything that follows. To understand why, here is what the actual tax law says and what the math looks like.

All scenarios below are hypothetical and illustrative. Verify with a CA for transaction-specific advice. Tax law cited is under Finance (No.2) Act, 2024, applicable from July 23, 2024.

Say a family acquired a significant painting privately at ₹40 crore through a dealer two years ago. No auction or public record. It sold publicly last week for ₹167 crore.

Scenario A - Sell at Auction (This Happens in India)

Under Indian tax law, paintings are explicitly capital assets under Section 2(14). Post Budget 2024, LTCG on paintings falls under Section 112 - taxed at a flat 12.5% without indexation. The holding period for paintings to qualify as long-term is 24 months (reduced from 36 months by Budget 2024 per CBDT FAQ). No ₹1.25 lakh exemption applies here - that is Section 112A, which covers listed equity only. The full gain on art is taxable.

Private acquisition cost (Year 0) ₹40 Cr

Public auction proceeds (Year 2+) ₹167 Cr

──────────────────────────────────────────────

Capital gain ₹127 Cr

LTCG @ 12.5% under Section 112 ₹15.9 Cr

Auction house commission (\~5%) ₹8.4 Cr

──────────────────────────────────────────────

Net proceeds, clean and documented ₹142.7 Cr

Effective conversion cost on gain ~19%

₹142.7 crore is now fully documented, tax-paid capital. It can go into listed equities, real estate, a PMS, or anywhere else.

For context: declaring ₹127 crore of undisclosed income under a tax settlement costs a minimum of 30% tax plus surcharge plus penalty, effectively 45–60% of the amount, with a permanent IT record linking you to unexplained wealth. Art gets you to the same outcome at \~19%, and the paper trail reads “sold a painting.”

Scenario B - What Does NOT Work in India

In the US, donating an appreciated painting directly to a museum allows the donor to claim a tax deduction at the painting’s current fair market value without selling, and without triggering capital gains. Donate at ₹167 crore, claim ₹167 crore deduction, pay zero LTCG. The math is extraordinary.

This does not exist in India.

Under Section 80G of the Indian Income Tax Act, deductions are available only on monetary donations - cash, cheque, or electronic transfer. Donating a painting in kind does not qualify for an 80G deduction. This is confirmed explicitly in IT rules. If you want the deduction, you must first sell the painting, pay LTCG on the gain, and then donate the cash proceeds, at which point the deduction only partially offsets the tax already paid.

This is one structural reason the Indian art market lacks the institutional museum-collector base that drives Western markets. The American tax incentive that turns billionaires into cultural patrons simply doesn’t exist here yet.

Scenario C - Pass It Down (This Works in India)

India has no estate duty - abolished in 1985. No inheritance tax either.

When the family holds the painting and the patriarch passes away, the collection passes to heirs under a will. Under Section 56(2)(x) of the Income Tax Act, assets received through inheritance or will are explicitly exempt from tax in the recipient’s hands. The heir’s cost basis resets to the declared value at time of inheritance - anchored to the last public auction price of ₹167 crore.

Gifts between living relatives - spouse, children, parents, siblings are also explicitly exempt under Section 56(2)(x). So a parent can gift a painting to a child during their lifetime with no tax liability in the child’s hands either.

Original acquisition cost ₹40 Cr

Declared value at inheritance ₹167 Cr

Estate duty payable Nil

Inheritance tax payable Nil

──────────────────────────────────────────────

Heir's cost basis resets to ₹167 Cr

Future LTCG computed from ₹167 Cr

(not from ₹40 Cr)

When the next generation eventually sells, say at ₹280 crore, their taxable gain is ₹113 crore, taxed at 12.5% \= ₹14.1 crore. Without the inheritance step-up, the gain would have been ₹240 crore, taxed at 12.5% \= ₹30 crore.

The family has permanently sheltered ₹127 crore of appreciation from ever being taxed - not through any scheme, just through the absence of estate duty and an inheritance exemption that has been in Indian law for decades.

In equity markets, Warren Buffett has called the equivalent US provision one of the most significant tax advantages available to wealthy families. In India, art achieves the same outcome for free.

What About Borrowing Against Art?

In the US, UK, and Switzerland, lending against art collections is a multi-billion dollar business - Bank of America, Citi, Sotheby’s Financial Services all run formal art-lending divisions at 50% LTV. Deloitte estimates global art loans outstanding hit $36 billion in 2024.

In India, no major private bank - HDFC, ICICI, Kotak, Axis publicly offers art-backed lending as a product. There is no documented, accessible product for this in India as of now. The structural logic is sound - pledging collateral triggers no capital gains event. But this is not yet a usable tool for Indian collectors the way it is in developed markets.

“But Wealthy People Still Buy Art in the US and EU After Regulation ?”

Fair point and the most important one to address.

Regulation didn’t kill those markets. Christie’s and Sotheby’s have had some of their strongest years since the EU tightened the rules in 2020. Serious collectors - institutions, foundations, diaspora buyers, genuine long-term investor never needed the opacity. Their money was already documented. KYC changed nothing for them.

What regulation actually removed was one specific use case: bringing in capital of unknown origin and running it through an auction without anyone asking questions. That’s it.

Scenario A still works after regulation - you still pay LTCG, the proceeds are still clean. Scenario C - inheritance has zero connection to AML rules. Estate tax is a separate legislative question entirely.

In the west, you can still pledge and borrow against art.

The only people genuinely inconvenienced are the ones who needed the opacity in the first place.

Which is probably why the art world lobbied against AML rules for fifty years and why, once the rules passed, the serious collectors barely noticed.

A Closing Thought

India’s art market is genuinely growing - $2 million in annual transactions twenty-five years ago, $338 million today, projected at $1.1 billion by 2030. Real collectors are entering. Diaspora money is returning. New museums are opening. The cultural story is not invented.

But markets that grow this fast, in asset classes this opaque, with regulatory frameworks this thin, tend to attract more than just art lovers.

The painting is beautiful. The price is a number. And numbers, in finance, always mean something beyond the obvious.

Note : This only for educational purpose. Not an advice or recommendation.

CompoundingAI is a vertical intelligence engine that transforms unstructured documents into decision-grade insights, complete with source-level traceability for confident, auditable workflows.

We cut the noise & directly deliver insights.

Powered by CompoundingAI — AI research platform for Indian stocks, every claim cited from primary filings

Login Now